Subtraction By Addition

I've recently dabbled in the topic of structure here on the blog. I'm a big believer in structure as a means to gain clarity, control, and momentum in the various aspects of our lives. A few readers asked me to provide an example as it pertains to everyday personal finance. Your wish is my command!

One of the primary principles I teach clients is the implementation of sinking funds. "Sinking fund" is formal name for a savings account with one particular objective. A car sinking fund would only be used to save for car expenses. A travel sinking fund would only be used to save for travel expenses. And so on.

Clients often look at me cross-eyed when, after ranting for 15 minutes about the importance of simplifying our finances, I introduce the idea of setting up a bunch of savings accounts. That seems counterintuitive. How can having more accounts help us streamline our finances?!?!

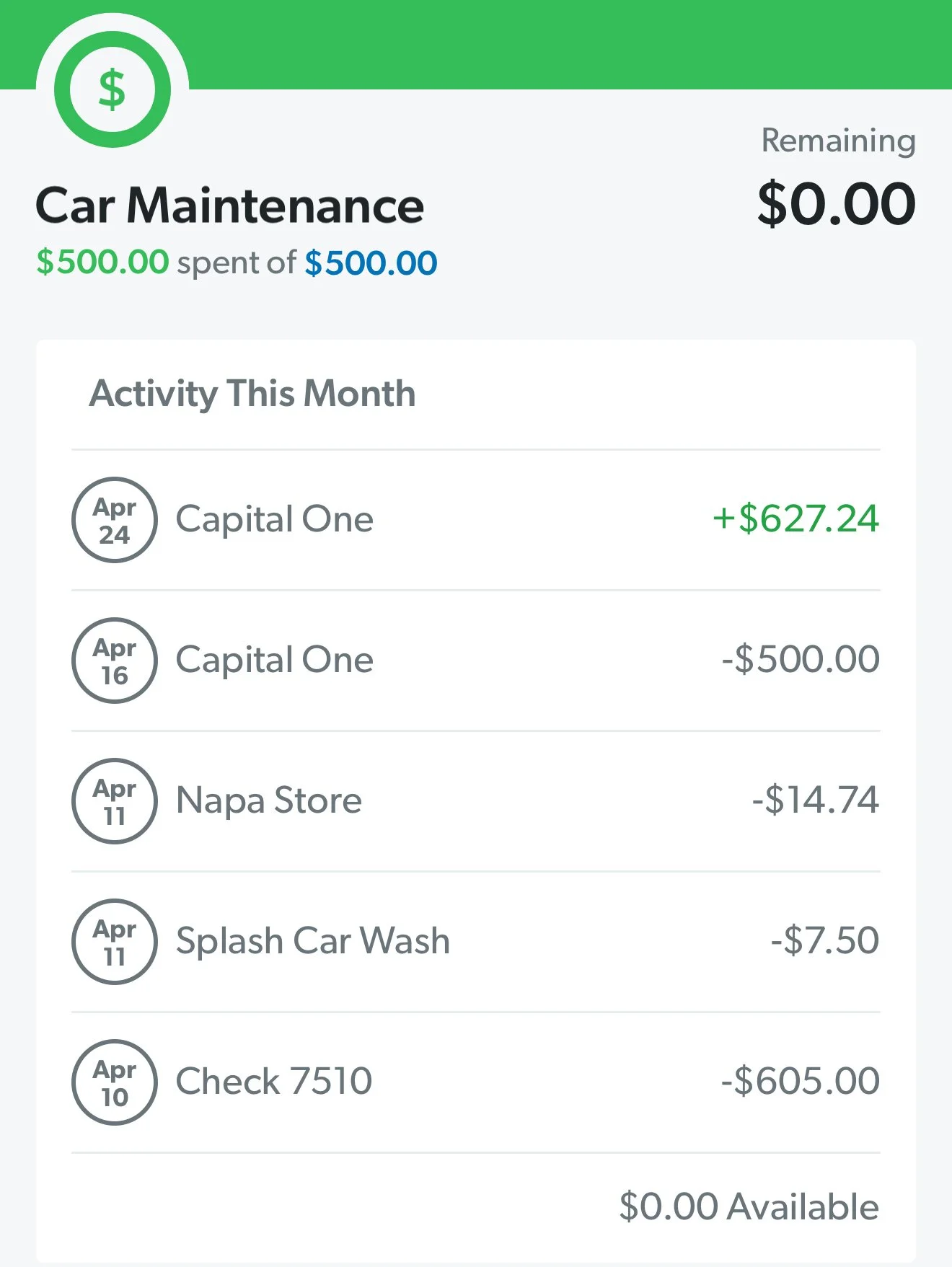

I have a sinking fund to pay for car maintenance expenses. It's a savings account set up at a bank, and it's creatively named "Car Fund." Every month, Sarah and I budget money for our car fund. After all, our cars WILL break down at some point. Oil needs to be changed. Parts need to be replaced. The last thing we need is a massive bill from our mechanic to blow up our month. Therefore, each month, without fail, we budget $500 in our car fund category. Then, like clockwork, we physically send $500 from our primary checking account into our car fund.

What this structure does is smooth out our car maintenance expenses. Each month, $500 goes into that account, where it (hopefully) builds over time. Then, when the dreaded car expense happens, it shouldn't impact our budget in the slightest. Here's a recent example:

As planned, $500 was automatically moved into our car fund on the 16th of the month. Three actual car expenses were incurred during the month: $605 to our mechanic, $7.50 for a car wash, and $14.74 for a part......a total of about $627. Knowing this, I reimbursed our checking account $627 from our car fund toward the end of the month. The net result of this is that we spent exactly $500 on car maintenance that month. Perfectly smooth, perfectly under control.

With that one piece of structure, we smoothed out what can otherwise be a brutally volatile category. Regardless of whether the mechanic's bill was $600, $1,000, or $2,000, our budget remains unchanged and unaffected.

Adding that one simple piece of structure actually simplifies our finances. It takes very little effort, and so much of our financial stress, tension, and anxiety can be thrown out the window. Perhaps this is a good week to set up a few sinking funds of your own!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.