The Daily Meaning

Take your mornings to the next level with a daily dose of perspective and encouragement to start your day off right. Sign-up for a free, short-form blog delivered to your inbox each morning, 7 days per week. Some days we talk about money, but usually not. We believe you’ll take away something valuable to help you on your journey. Sign up to join the hundreds of people who read Travis’s blog each morning.

Archive

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- August 2021

- November 2020

- July 2020

- June 2020

- April 2020

- March 2020

- February 2020

- October 2019

- September 2019

It’s Hard to Overcome Our Structure

Unfortunately, it's hard to overcome our structure. This family had created a really expensivefinancial structure for their household. Based on THEIR choices, more than 70% of their income was already spoken for before it hits their bank account. No amount of trimming or cutbacks can help this family remedy what ails them.

Someone contacted me with a problem. A couple in their mid-40s, two kids. They believed they were being responsible with their money, but it felt nearly impossible to make financial progress. As they put it, they didn't waste money, spend money frivolously, or buy nice things. Yet, they lived month-to-month and had much financial tension in their marriage.

I sat down with them to review their numbers. Here's what I found (shared with their permission):

Combined Take-Home Income: $8,200

Mortgage Payment: $3,600

Car Payments: $1,600

Other Debt Payments: $700

Do you see a problem here? Just their house payment is 43% of their take-home income. The house plus the cars account for 63%. Then, when you tack on the rest of the debt, these three categories account for 72% of their take-home income.

That means they only have $2,300 left for all other needs, wants, giving, and saving. That's not nothing, but wow, it's tight. So when they say they don't waste a bunch of money or spend frivolously, I believe them. There's no money to waste!

Here was their question: "How do we find margin? Where do we cut?"

These are tough situations. Unfortunately, it's hard to overcome our structure. This family had created a really expensivefinancial structure for their household. Based on THEIR choices, more than 70% of their income was already spoken for before it hits their bank account. No amount of trimming or cutbacks can help this family remedy what ails them.

Whether we want to admit it or not, these are OUR choices. The cities we reside in. The residences we choose. The cars we buy. We can cry foul all we want, but at the end of the day, we have choices to make; and these choices will dictate our structure.

Here's what happened. I pointed out that there are very few options to help this family without them significantly altering their structure. They can't cut groceries, utilities, dining out, clothing, entertainment, or any other budget items enough to move the needle. It's hard to overcome our structure! I couldn't let them go home empty-handed, though. Here are the options I floated by them:

Increase their income

Downsize their residence

Sell one or both vehicles (and replace them with cheaper alternatives).

Use some of their assets to pay off their non-car and non-mortgage debt.

Outside of these four levers, very few options exist to help them. Their structure is their structure, and it must be addressed for what it is. It's tough, but reality.

I hope this family takes a hard look in the mirror and decides to take drastic action; only time will tell. I sincerely believe their life will unlock if they are willing to humble themselves and make difficult choices.

The same goes for you....and me. We can trim around the edges all we want, but our financial structure significantly impacts our journey. For some of you, it may be time to alter your structure.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Being Responsibly Irresponsible

On the one hand, I repeatedly beat on the drum of values-based spending, investing in memories, and finding meaning in our finances. Then yesterday, I leaned into this idea that we shouldn't impulsively spend "extra" money that comes into our lives. Instead, we should apply all extra income to wherever we are in our plan. See the possible incongruency here?

As is the case most days, I opened my Daily Meaning e-mail inbox yesterday to find a message from my friend Randy. Randy consistently responds to my blog posts, including words of encouragement, a representative story, additional wisdom, or alternative perspectives. Yesterday's was a bit different. He pointed out that some readers might find yesterday's post (about not impulsively wasting extra money) incongruent with my typical message of using money on "spending for memories and meaning." He didn't personally find it incongruent, but he suspected others would......and he was right. I subsequently received a handful of questions and responses indicating such.

On the one hand, I repeatedly beat on the drum of values-based spending, investing in memories, and finding meaning in our finances. Then yesterday, I leaned into this idea that we shouldn't impulsively spend "extra" money that comes into our lives. Instead, we should apply all extra income to wherever we are in our plan. See the possible incongruency here?

Here's the bridge for this perceived gap: responsibility and intentionality. It all comes down to those two things. If we don't take responsibility for our finances (pay for needs, save for future expenses, and give), our finances get disjointed.....and stressful! Yes, we should use some of our money for fun and memorable things. However, having our financial ducks in a row is a must. If we're behind on rent, can't put food on the table, and the utility companies threaten a shut-off, we probably shouldn't be dumping our money into lots of wants (today). We need to solidify the foundation. Responsibility is critically important!

Second, intentionality. As I often mention, I don't personally care where you choose to allocate your money. People have different values, priorities, passions, and situations. It's inevitable that your "right" is different from my "right." Here's the second part of my slogan. I don't personally care where you choose to allocate your money......as long as it's intentional. It's planned. It's purposeful. It fits within the context of our broader finances. With intentionality comes peace; with impulse comes regret.

Three of my clients recently traveled to Europe for some epic summer trips. Believe me, I've been living vicariously through them all summer!!!! The pictures are beautiful, and I suspect the memories are much sweeter. Each of these trips cost them anywhere between $6,000-$14,000. That's a lot of money, but they put a ton of intentionality into it. Some of these families have been saving this money for years. Month after month after month of saving. Then, the planning. They got the flights, then the hotels, then started filling the days with museums, trains, tours, and restaurant reservations. So much intentionality! By the time the trip arrived, they had zero financial stress and, carried themselves confidently, knowing their overall finances were intact and thriving.

Let's call this living responsibly irresponsible. Do the things other people judge you for. Make them roll their eyes. Let them question your sanity. But behind the scenes, do it with much intentionality and responsibility.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

It’s a Slippery Slope

See the problem here? Whenever we treat something as "extra" or "different," we undermine our finances and marriage. We go from "ours" to "mine." From "being responsible" to "screw it." It gets muddy.

In yesterday's post, I referenced how money is fungible. All there is is money in, and money out. This money doesn't go here, and that money doesn't go there. We have income, and we have outflows. Period.

Typing that reminded me of a situation that played out early in my marriage. Sarah and I were in the midst of our journey to pay off $236,000 of debt (it sucked as much as you're thinking). We each received a little personal spending each month, plus a few other fun expenses like modest dining out and travel. Then, every other excess dollar we had went toward the debt.

One day, Sarah decided to add a part-time nannying gig to her schedule. As we ate dinner, she started verbally processing what she might want to do with this extra income. Maybe clothes. Maybe nails. So many fun options!

That's the moment, mister fun hater (me), stepped in. I shared with her that money is fungible and, as such, this extra income had to be two things:

Ours, not hers.

Included in our budget.

She was noticeably annoyed with me. After all, she was the one working extra hours to earn this extra money.

She explained that our paychecks were our budget money, and this new income was "extra." (You know what we do with extra, right?) And since it was extra, it should fall outside of our budget and she should be able to do anything she wants with it.

Me: "Oh interesting. In that case, I'll have to figure out what I want to spend my annual bonus on!!!!"

Her (even more annoyed): "Your bonus is part of your work, so it's different." (I'm paraphrasing here, as I don't remember her actual comment)

Me: ......

See the problem here? Whenever we treat something as "extra" or "different," we undermine our finances and marriage. We go from "ours" to "mine." From being intentional to "screw it." It gets muddy…and messy.

Sarah eventually saw my point. I was grateful for her desire to work harder to help our young family dig out of a hole, but income is income. Ultimately, here's where we landed. We included her nanny income in the budget as income, juiced up her personal spending a bit, and added the to the debt paydowns. It was a win-win.

It's a slippery slope to treat money as anything but fungible. All there is is money in, and money out. Remove impulses. Take out the bias. Don't undermine your relationship. Don't sabotage your finances.

We've never had an issue with that topic since that day nearly 13 years ago. I may make 99% of our family's income, but it's "ours." Never "mine." Never. Don't fall down that slippery slope!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Let Blessings Remain Blessings

What do you typically do if you receive unexpected extra money? If you're a human (and I suspect you are), there are two typical outcomes.

I opened the mail yesterday to two unexpected blessings: two checks I never saw coming. I'm not talking about massive amounts of money here—$250 and $100.

What do you typically do if you receive unexpected extra money? If you're a human (and I suspect you are), there are two typical outcomes:

The most common outcome is to simply blow it. It's extra, and most of the time, we don't respect those extra blocks of money. It will likely be impulsively spent before the check even clears.

The second most common outcome is to dump it into a general savings account, which will be hoarded in the near term and probably impulsively spent at some point in the future.

I prefer to let blessings remain blessings. First, I don't actually care what you do with it. Whether you spend it, save it, or give it is not what's important in this conversation. Here's what I do personally, and it's how I coach it every single time:

Add this as income to your budget. If it's money coming in, whether it's a $100 reimbursement check or a $10,000 bonus, it's income. Add it to the budget as such.

Once it's in the budget, you have $x more in the budget than you did before. Let's pretend it's $200. You add the $200 as income to your budget, giving you $200 more to allocate somewhere in the realm of spending, saving, or giving. Treat it as you would any other $200 in your budget. $200 is $200.

As such, allocate this money in accordance with your current plan. If you're in the midst of paying off debt, pay off more debt. If you're saving for a big trip, save more for your trip. If you've been working on a financial gift to your favorite organization, give it.

Execute the plan. If you say you're going to do something, do it. After all, you promised yourself in your budget. Own that. If you plan to buy a new espresso machine, buy the machine! If you plan to pay off that credit card, pay it off! Don't break your promise to yourself.....or your spouse.

That's the thing about money, it's fungible. All there is is money in, and money out. The moment we try to say this is for that, and that is for this, we've lost the plot. Instead, look at everything as one big puzzle. When we do that, we develop a much healthier and more productive relationship with our money. No guilt, no emotional strings, no sense of obligation. Just wisdom and discernment.

As for us, August has been a kid-expense-heavy month. Activity fees, school supplies, new shoes, and end-of-summer fun have drained that category quickly. I suspect Sarah and I will pad that category with this unexpected windfall. That's our current reality, and we'll live into that.

Meet your money where you are. Don't waste these little (or huge!) opportunities. Let your blessings remain blessings.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Two Is Better Than One

Ownership and action are two different things. Yes, both spouses need to have ownership. However, couples don't need both spouses to jointly manage the finances. There are so many different ways this can play out.

I regularly discuss how married couples must take joint ownership of their finances. It's critically important that both spouses are involved. Today, though, I want to clear up one common misconception.

Ownership and action are two different things. Yes, both spouses need to have ownership. However, couples don't need both spouses to jointly manage the finances. There are so many different ways this can play out.

For example, one spouse may pay all the bills, and the other handles all insurance and investments. Another example is having both spouses jointly pay all the bills and manage the budget together (they literally sit at the table together and work through it together). Both of these approaches are perfectly acceptable, but here's my broader point. It doesn't matter who does what, as long as both spouses have a voice, ownership, and accountability.

I'll use my marriage as a third example. I'm married to a woman who is allergic to numbers. Trust me, it's been scientifically proven. Sarah has zero interest in bills, investments, insurance, or anything else that includes dollar signs and numerical digits. And that's okay! What's important is that Sarah has ownership.

Each month, Sarah and I discuss, negotiate, and set our budget. Some months are more difficult or busier than others, but that's been our general trend for nearly 15 years. I may make 99% of our family's income, but she has an equal voice (it's "our" money, not my money). Her opinions matter. Her influence is imperative. We negotiate what will happen with our money, and then she turns the management over to me. She has her own role, though. Since she has ownership, she's accountable for living out the plan we set for our family. She must honor the budget we set together and execute whatever life decisions come with it. But I handle 100% of the actual financial management. That approach is okay, too!

That's ownership vs. action. There is no right or wrong. Some couples do everything together, some have a clear delineation of duties, and some are like mine, where one spouse does most (or all) of the management. All of these are acceptable approaches, under one condition: both spouses have ownership.

If your spouse doesn't have ownership, accountabiity, engagement, or a voice, I encourage you to bring him/her into the fold. It will lead to more financial success, an improved marriage, and a reality where your finances become an extension of your values, dreams, and aspirations. In other words, it changes everything!

The Blink of An Eye

A little more than eight years ago, Sarah and I were a mid-30s couple who aspired to one day have children. Just a handful of days later, we were the parents of twin baby boys. We went from “we wish” to “oh crap” in about twelve seconds. We bought car seats, bottles, clothes, and diapers AFTER meeting them for the first time. We didn’t even have a room ready for them. Our lives forever changed in the blink of an eye.

A little more than eight years ago, Sarah and I were a mid-30s couple who aspired to one day have children. Just a handful of days later, we were the parents of twin baby boys. We went from “we wish” to “oh crap” in about twelve seconds. We bought car seats, bottles, clothes, and diapers AFTER meeting them for the first time. We didn’t even have a room ready for them. Our lives forever changed in the blink of an eye.

For as much as we think we have a firm grasp on our lives, reality often plays out differently. Birth, death, job loss, marriage, sickness, career shifts, divorce....all sudden forces that have the power to change our lives in the blink of an eye. There’s a problem, though. When we think we have a firm grasp on our lives, we act as though we have a firm grip on our lives. In the financial arena, it typically means that we create our personal cost structure that works for one reality: the present one.

I often meet with couples who were feeling fairly confident in their finances for years, until _____ happened last month. As long as their family is healthy, employed, and not making any changes, they can keep the train on the tracks. However, when we structure our life so specifically, it doesn’t allow margin for life to happen.

It reminds me of a situation that still haunts me to this day. Many years ago, I was meeting with a couple. Two strong careers, no kids. They lived in a beautiful home, drove luxury cars, and took exotic trips. Between their hefty mortgage, two obscene car payments, and a glitzy lifestyle, their monthly expenses absorbed most of their income. I asked them about kids. I recommended they start making some shifts in lifestyle to create margin for changing circumstances. Namely, I suggested they consider what-if scenarios that may include one of them working part-time or staying home completely. Before I could finish, the wife snapped at me, “I’m not staying home. Zero chance!” They completely shut that conversation down. Over the next few meetings, I tried to bring it up again, pointing out that sometimes, but not all the time, having children shifts career aspirations and jumbles priorities. Again, they were adamant there’s zero chance of either staying home. Thus, they continued down the same path.

Fast forward 18 months, and they gave birth to a beautiful baby. Then comes our next coaching session. Wanna guess what the topic of conversation was? The wife, now a mom, was desperate to stay home with her baby. Life changed in the blink of an eye, but they structured a life that works for just one reality. When I visually showed them there was no way she could stay home (or even work part-time) without completely gutting their lifestyle (house, cars, travel, etc.), there were a lot of tears. So sad!

Life can change in the blink of an eye. Knowing that, it’s imperative that we structure our life in a way that allows us to shift with it.

The Three-Month Rule

Budgeting is simple—eventually. Budgeting is powerful—eventually. Budgeting is a game-changer—eventually. Budgeting isn't something we just pick up and are magically good at. After all, if you don't budget, there's a strong likelihood you've operated your finances without one for years....maybe decades. So we can't expect to be overnight experts.

Happy last day of the month. How in the world is the year half over?!?! Today also marks a special occasion. Being thelast day of the month means tomorrow brings a brand new budget. If you're a budgeter, you know exactly what I'm talking about. It's a day that brings hope, possibility, and excitement. It's a new opportunity to bring our values to life through our finances. For some of you, it's also a great opportunity to close the book on a really crappy month and start afresh. Either way, tomorrow is your day!

If you're not a budgeter, perhaps July is your month to begin. Whenever I talk to people who don't budget, I ask, "Why?" There are a million reasons people don't budget, but there are a few common responses:

"It doesn't work for us."

"I suck at it."

"It was too hard to follow."

"I didn't like it."

All of these are valid reasons, but on the flip side, they are probably (half) wrong. Budgeting is simple—eventually. Budgeting is powerful—eventually. Budgeting is a game-changer—eventually. Budgeting isn't something we just pick up and are magically good at. After all, if you don't budget, there's a strong likelihood you've operated your finances without one for years....maybe decades. So we can't expect to be overnight experts.

Whenever coaching someone on their first budget, I always add, "you're probably going to fail." Encouraging, I know! But it's true. The first month, or two, or even three will probably be a mess. The goal isn't to crush this budgeting thing in the first month, but rather experiment, learn, and grow. What works. What doesn't. What abc category costs. Why xyz category needs to be changed. How to better track. How to engage our spouse better.

The problem for most prospective budgeters is they don't do a great job the first month, feel like trash about it, and simplygive up. You're supposed to fail! That's all part of the game. I call it "the three-month rule." Those first three months will be tough, but it's the setup for what's to come. Typically, by the fourth month, most people are fairly locked in and confident to execute on their plan.

That's my encouragement to you today. If you don't budget, I encourage you to give it a try, give yourself grace, know you're going to mess up, and know it's going to get better. If you give it at least three months, I strongly believe it will become a valuable tool in your financial arsenal.

And remember, budgeting isn't about spending less; it's about spending better. It's about harnessing every dollar of income you're blessed with this month and aligning it with your values. Spend, save, and give in accordance with YOUR values.

Happy new budget month, y'all!

The Clamps Are Tightening

Do you ever feel like you make good enough money and manage it well, yet there's simply no margin in your financial life? If so, you aren't alone. Millions of families in this country are experiencing this phenomenon.

Do you ever feel like you make good enough money and manage it well, yet there's simply no margin in your financial life? If so, you aren't alone. Millions of families in this country are experiencing this phenomenon. Inflation has wreaked havoc on so many people. What not long ago felt like a respectable income has turned into "just scraping by." Even though inflation is going down, its consequences are here to stay. This is a common misconception about inflation. When inflation goes down, it doesn't mean prices go down. Rather, it means prices are going up less quickly from their now-inflated levels. It's a mess.

I regularly meet with families that make $8,000, $10,000, or $12,000/month of take-home income, barely making ends meet. Much of this can be attributed to the cost structure established by the family prior to inflation setting in, which is difficult to change. It's embarrassing for people, and they feel alone. After all, it's weird to tell your friends or family members, "Yeah, I know we make $160,000 per year, but we're really struggling." That sort of conversation will make people play their miniature violins with their eyes rolling. Therefore, people suffer in silence.

It feels like the clamps are tightening. We can stave off the financial pressure for a while, but eventually, it starts to add up. The normal life costs keep increasing until they've squeezed out the margin. One-off expenses, such as medical bills, car maintenance, and house repairs slowly bleed people dry. We make purchase decisions that entrap us in debt. We experience shocks to our income. One by one, families are breaking.....it's so sad!

If any of this hits home for you, perhaps what I'm about to say next can help you relieve some of your pressure. Here is a menu of options to help you navigate a tight financial season:

Find areas of your monthly budget to cut. You may need to trim down on dining out, travel, or other wants.

If you have assets tied to debt (and hefty loan payments), you might consider selling them. One of my clients sold their vehicle, and it immediately freed up $800/month from the car payment being done.

Temporarily tone down your investment contributions.

Temporarily stop saving toward your sinking funds. Yes, these are important, but it's more important to keep the financial train on the tracks.

Find extra income. A side hustle or side job can relieve a ton of financial pressure.

If you're not sitting on a cheap mortgage, it might be time to downshift your housing.

You aren't alone! But at the same time, the burden of navigating it is on you. I don't like it any more than you do, and I think we have some major problems on our hands, but it's the reality we're stuck with (for now). We must face it head-on so our families can live to fight another day. It's a tall order, but you got this!

I'm happy to chat if you have any questions about your own situation. This is a scary and prevalent issue, and you don't need to face it alone.

5-Star Dining at a 2-Star Establishment

While I love a 5-star restaurant as much as the next person, not all meals need to be profound. Sometimes, it's just about creating memories over some simple food. The food was just that: simple. However, we had a blast together, and everyone walked out happy and full.

I hope all the dads and grandpas had a wonderful Father's Day yesterday. We made a quick trip to my parents' house for the weekend, where my dad and I spent Saturday doing body work on my new car. The car is in pretty good shape overall, but 18 years of life has provided a few scrapes and scars along its journey. Here’s an updated pick after removing the chip guard film and restoring the headlights.

We drove home yesterday morning so I could coach Finn and Pax's last soccer game of the season (and they won the league championship!). It was 90+ degrees out, so we grabbed some ice cream afterward, and then took a wonderful nap. To finish the night, we had a little Father's Day dinner out.

IHOP. Yes, IHOP. It's not my favorite place in the world, but the family was craving breakfast, and they have a kids-eat-free special. We had a great time together, and it was the perfect way to cap off a great Father's Day.

While I love a 5-star restaurant as much as the next person, not all meals need to be profound. Sometimes, it's just about creating memories over some simple food. The food was just that: simple. However, we had a blast together, and everyone walked out happy and full.

Over the years, our dining out budget has varied. During our pre-kid debt payoff years, the budget was $100/month. During our pre-kid post-debt years, the budget was at least $500/month (we had a lot of fun dining in that season!). After the twins were born, our dining out dropped to around $200/month (a few nice date nights). After I left my prior career and we took a 90% pay cut to start over, it went back down to about $100/month. Today, we're in the $250/month range.

We NEVER deviate from the budget. If we have money left, we use it. If we don't we don't. It's one of the ways Sarah and I show commitment to our budget, which we negotiate and agree upon at the beginning of each month. We don't exceed it....no exceptions. Sometimes, that sucks. Sometimes, it's frustrating to be 20 days into the month with no dining out remaining. But that's on us. That's our fault. That was our mistake; therefore, it's our burden and consequences.

That level of self-discipline changes things. It forces us to make wise decisions. If we can't bend the rules, then we must find a way to live within the rules. We can always create new rules next month, but this month's rules are this month's rules. Sometimes that means we get to eat at a Michelin-starred restaurant, and sometimes we eat at IHOP. Both are wins, by the way.

That's the beauty of setting financial guardrails in our lives. It's not something we have to do, but rather something we get to do. Once the rules are set, we have the creativity to work within them with no guilt, no regret, and no remorse. Freedom through boundaries.

Good Morning, Bob Ross

Hello, Bob Ross! Yes, you! You're an artist, you know. Today is the first of the month, which means you woke up to a blank canvas. Whatever happened last month is gone....it's on that old, messy canvas. My May canvas was a disaster. We had surprise expenses, mishaps, and oversights. We screwed up. I didn't like the painting we ended up with.

Hello, Bob Ross! Yes, you! You're an artist, you know. Today is the first of the month, which means you woke up to a blank canvas. Whatever happened last month is gone....it's on that old, messy canvas. My May canvas was a disaster. We had surprise expenses, mishaps, and oversights. We screwed up. I didn't like the painting we ended up with.

But today? Today we each wake up with a clean, white, beautiful canvas. For the next 30 days, we'll curate a new piece of art. We'll make money, spend money, save money, give money, and invest money. Thousands of transactions and events will slowly paint the canvas, stroke by stroke.

We have two choices today. We can either grab brushes and haphazardly begin tearing across the canvas with reckless abandon, or we can make a plan. Many people attack their clean and beautiful canvas with chaos, reactivity, and urgency, resulting in crazy artwork akin to what my toddlers used to bring home from pre-school. Others will take a few minutes before picking up a brush to determine the objective of this potential masterpiece. Where the trees will go, how fluffy the clouds will be, and where the water meets the horizon. No, it won't be perfect; perfect doesn't exist. But when the painting is complete, it will be beautiful.

Here's my encouragement for you today:

Reflect on what happened last month: the good, the bad, and the ugly. Learn from it. Celebrate the wins and forgive yourself for the losses.

Put the past behind you. You can't drive forward by staring into the rear-view mirror. That's a recipe for a disastrous crash. Eyes forward!

Take 15 minutes to create a plan for your money money. How much is coming in, and from where? What are your needs? What debts need to be paid? How much will you give? Make sure to add some fun in there. Determine which saving initiatives need attention. Make sure every dollar of income has its marching orders. No soldiers left behind. Each is important.

Commit to yourself (and if relevant, your partner) to follow your plan. After all, it's your plan.

Execute with confidence and conviction. Paint that canvas!

Repeat the same process next month.

This money stuff can suck. It can be the source of so much pain, suffering, turmoil, and tension. But if done well, it can also lead to some beautiful places. Perfect, no. Beautiful, yes. Instead of viewing it as dollars and cents, see it as bringing your values, aspirations, and meaning to life. Treat it like a blank canvas, just waiting for a Bob Ross masterpiece to be painted. Your masterpiece.

Just Move One Piece

With as complicated as our finances can become, there are a lot of moving pieces. Sometimes, families feel the need to adjust every number every month. They try to focus on all the categories and prioritize everything, then get overwhelmed. Instead, I encourage people to "just move one piece."

Finn recently decided to be a chess player. It was an unexpected development in our household, but I dig it. I'm not good at chess, but it's fun to compete with him and watch his little brain work. In the first few games, I had to remind him, "just move one piece." You move one, I move one.

With as complicated as our finances can become, there are a lot of moving pieces. Sometimes, families feel the need to adjust every number every month. They try to focus on all the categories and prioritize everything, then get overwhelmed. Instead, I encourage people to "just move one piece." If there are one or two categories that we need to get better control of, focus more dollars to, or gain more intentionality on, put your energy there.

We shouldn't try to do everything. If we can hone in on one or two things this month, then maybe we can grab another next month. Music lessons and cell phone replacements are two categories for us. After a trial run for drum and electric guitar lessons for the kids, it's time for Sarah and I to build that expense into our budget for the foreseeable future. That's a priority for us, and we need to create margin and consistency with it.

Second, Sarah's phone is in hospice care. We need to make quick decisions, or she'll be living in 1994 again. Therefore, we'll lean hard into this category and find a way to replace her phone quickly.

It's the power of the just moving one (or two) piece(s). We can't move the needle on every goal, every category, and every habit. But we can move the needle on a few, then next time a few more, then eventually a few more.

As one more visual, let's say you have five different priorities, each costing $500. Let's also pretend you have $500 of monthly discretionary income after all needs, wants, and giving have been accounted for. If you prioritize them equally and try to do everything at once, you'll contribute $100 to each of them. At that pace, it will take five months to achieve a win. On the flip side, if you decide to prioritize just one (and contribute all $500 to it), you accomplish a goal in the first month. If you do the same in the second month, you achieve another goal. Constant momentum.

Many financial situations in our lives involve this principle. If we just move one piece, we can move the needle quickly while gaining confidence from the wins.

The new month is quickly approaching. What one (or two) piece(s) will you move?

One At a Time

At that moment, I triggered my motto, which I find helpful when these anxious feelings creep in: "One at a time." I can't categorize 68 transactions at once, but I can categorize one....then one.....then one.

Yesterday, I faced the same challenge many of my clients regularly encounter. After a few weeks of travel, sickness, and the Northern Vessel car crash sequel, my personal finances have taken a back seat to life. This is a natural consequence when life gets busy. It's not a matter of if, but when. Life WILL get crazy, and when it does, our finances may be a temporary victim.

Upon finally having a little spare time on my hands yesterday, I popped open my budgeting app to see what things looked like. Much to my despair, I was met with 68 uncategorized transactions. Crap! Few things cause anxiety and overwhelmingness quite like realizing you've fallen that far behind on tracking your finances.

At that moment, I triggered my motto, which I find helpful when these anxious feelings creep in: "One at a time." I can't categorize 68 transactions at once, but I can categorize one....then one.....then one. Here's how my brain works when starting my one-at-a-time process:

First, I start with the most recent transactions, as they are most likely fresh in my mind. I quickly categorize each item that's immediately familiar.

Second, I scan the transactions for vendors that are obvious categories. MidAmerican Energy is electricity. PureBarre is Sarah's fitness. Leaning Tower Pizza is dining out. Simple and clear.

Third, I choose a vendor that has multiple transactions popping up, and systemmatically knock out each transaction. Amazon is a great example. I had about a half dozen Amazon transactions. I logged into my Amazon account, scrolled through my recent orders (to determine what categories each transaction entailed), and categorized each transaction accordingly. I repeated this process for Target and Wal-Mart transactions by using their respective apps.

Fourth, after working through the first three steps above, my unallocated transactions shrunk from 68 to 15. These remaining transactions take a bit more work. They may involve a quick conversation with Sarah, an e-mail search for receipts, or logging into my bank account to see if there's an expanded transaction description. These are never fun, but it's a lot easier when there are only a handful of them.

One at a time. This is such an important perspective when dealing with our finances. Things can get complex and overwhelming. It's the nature of money and numbers, which is why so many people flounder or just give up. But when we take a one-at-a-time approach, nothing is overly intimidating. Just keep moving forward. Sure, we'd love to be sprinting every step of the way.....but even a crawl is still progress. Putting one foot in front of the other.

Apply this to all areas of money—heck, apply it to all areas of life! Break things down into digestible chunks. Make it approachable. Create opportunities for small wins. Execute. Repeat.

It feels good to get caught up on my budget tracking and again have clarity on where we stand. I'm sure I'll get derailed again at some point, but when I do, one at a time!

Plug the Leaks

It's interesting how our instinct is often to cut back on the most prominent (and important) things in our lives. These families aren't alone! We all do it to some extent. I suspect one of the reasons we do this is because those prominent things are front and center; they are obvious.

"We need to stop spending so much on dining out."

"We need to cut back on travel."

"We need to quit going to games."

These are three comments made to me in the past few weeks. They are from three separate clients, each with their own financial tensions. Things feel tight. There's not enough margin to keep the train on the track, never mind make financial progress. Their natural inclination is to cut back, which is fair. However, I think they are sniffing up the wrong tree.

The first family's love language is food. Going out to eat is one of their biggest bucket-fillers.

The second family's passion is travel. It's their #1 priority, and it fuels them.

The third family are avid sports fans. Watching their teams play is one of their unifying and family-centric hobbies.

It's interesting how our instinct is often to cut back on the most prominent (and important) things in our lives. These families aren't alone! We all do it to some extent. I suspect one of the reasons we do this is because those prominent things are front and center; they are obvious.

Here's what I think. I think it's prudent for these three families to cut back. However, I think cutting back on these suggested categories would be counter-productive and possibly detrimental. Instead, I recommend they find the leaks.....and plug them. Oh, there are always leaks! They have them, you have them, and I have them. Expenses (big or small) that are either redundant or fail to add value to our lives.

A subscription for a streaming service that we don't watch.

A membership for a gym we don't even use.

Extra product that we won't use or will ultimately go bad.

A loan payment (plus insurance, maintenance, etc.) for a vehicle rarely driven.

Instead of indiscriminately cutting some of these families' most valuable expenditures, we looked for leaks. Here's what we found: One family found $300 of monthly leakage, another found $650, and the third found $1,700!!!

With very little effort, these families were able to recoup this cashflow in their monthly budget, which reduced their financial tension. It also prevented them from having to cut back on the things they value most. Huge wins!

Plugging the leaks is so powerful! Maybe you have some leaks. I suspect you do. I challenge you to find them, plug them, and use that found money for things that truly add value to your life!

Move the Decimal Left

Far too often, we burn ourselves out by dwelling on the minutiae. We spend so much of our time and energy trying to get the tiny details right that we lose sight of the big picture. Some of you know exactly what I'm talking about!

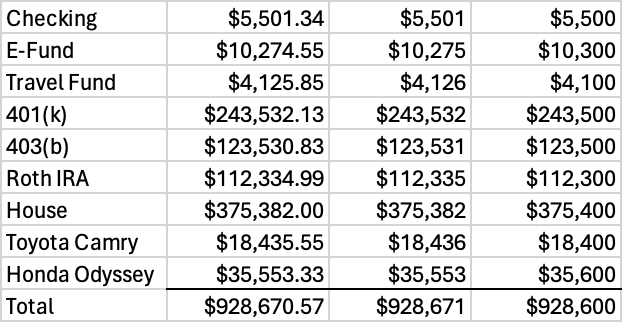

$4,125.85

How do you read this number? The correct answer is four thousand, one hundred twenty-five dollars and eighty-five cents.

The better answer is forty-one hundred dollars.

16 syllables vs. 7 syllables.....and a whole lot of noise.

Whenever I work with clients, my mantra is simplify, simplify, simplify. I don't deal with precise numbers. When logging monthly budget numbers, I round to the nearest dollar. I've never once used cents, and I never will. Whenever I log assets and debt on a net worth statement (which happens every meeting for every client), I round to the nearest hundred dollars. Yes, hundreds. Here's an example:

Let's compare the three columns. The leftmost column represents the precise answer. The middle column shows the figures rounded to the nearest dollar. The rightmost column displays the figures rounded to the nearest hundred. Now, which column do you find the easiest to comprehend, visualize, and discuss? Undoubtedly, it's the right column! This simplified representation not only makes financial data more readable and digestible, but also empowers you to have more meaningful discussions about your finances. It might ruffle the feathers of my accountant friends, but that's just a little bonus treat for me!

Far too often, we burn ourselves out by dwelling on the minutiae. We spend so much of our time and energy trying to get the tiny details right that we lose sight of the big picture. Some of you know exactly what I'm talking about!

Confession: I haven't balanced my checking account in over 30 years. I intentionally budget each month and track what happens. I can tell you how much I've spent on gas over the last 15 years, but it's not a precise number. However, it's a correct number. Why? When we round thousands of transactions, the laws of probability tell us that half will round up and half will round down.....meaning it will all work out in the end. If I were to reconcile five years of my personal finances, I suspect my margin of error would be a fraction of a fraction of a percent......you know, a minuscule rounding error.

Is it perfect? No. But it's sustainable, digestible, and repeatable. If I had been obsessed with pennies in my budgeting process, I would have quit 15 years ago. Instead, I simplify, simplify, simplify. My process is clean, easy, and user-friendly.

I can't even tell you how many people I've worked with who insisted on getting everything perfect down to the penny, only to burn out and quit mere months later. This money stuff doesn't have to be rocket science. It should be simple, but it can only be simple if we make it simple.

Here's my encouragement for you today. Move that decimal point left! Don't zoom so far in that you miss the big picture. If using round numbers helps you understand and execute your money better, more power to you. Don't aim for perfection. Aim for progress!

Planned Impulsiveness

Some people are planners, and some people are impulsive. Both have pros and cons, but impulsive people are known for self-sabotage and occasional (or frequent!) irresponsibility. I

One of my favorite Meaning Over Money podcast episodes is called Planned Impulsiveness. It was our fifth episode, released more than three years ago. Unfortunately, Apple lost our first 15 episodes like my kids lose their shoes. Other platforms managed to keep track of them, though. Despite being missing from Apple for over two years, it's one of the ten most downloaded episodes we've ever had. You can find it HERE.

The premise is simple. Some people are planners, and some people are impulsive. Both have pros and cons, but impulsive people are known for self-sabotage and occasional (or frequent!) irresponsibility. I'm oddly wired for both. I'm very impulsive, but I'm also a planner. Along my financial journey, I realized I needed to harness my impulsivity and turn the cons into pros.

This is where the structure comes in. Travel is a great example. I have a separate bank account specifically for travel. Each month, we budget approximately $1,000 for it. We may not travel every month, but we treat it as an expense. That $1,000 physically gets moved from our primary checking account and into our travel fund. The money slowly builds over time. Then, when it's time to travel, we travel. Sometimes, the travel is planned well in advance, and sometimes, it's more impulsive. In either scenario, the money is there, just waiting to be spent on travel.

I'll share my favorite (least favorite) story of my life. In the summer of 2016, Sarah and I were about to become parents. After a long adoption journey, we received word that our son was born. We went to bed with anticipation, excited to meet our little man the following day. As I was wrapping up a few things at work the following morning before getting on the road, I received a phone call. I immediately knew something was wrong. The following 30 seconds were the worst of my life, as I found out we lost our son.

Needless to say, the subsequent days were absolutely miserable in our house. Sarah was an absolute wreck, and I wasn't in a great position to hold her up. A few nights later, she told me she wanted to leave. Somewhere far, far away from our life. At midnight, I booked flights to Cancun and reserved a hotel room. We packed a few bags, took a nap, and drove to the airport five hours later. We spent the week crying, mourning, and eating our weight's worth of chips and salsa. It was terrible, but it was beautiful. It was impulsive, but it was planned. I'll always be grateful for that sad but memorable week with Sarah.

One of my clients recently had their first planned impulsiveness moment. They've been intentionally budgeting and using their travel sinking fund since December. Then, it happened! A significant event suddenly popped up, and they wanted to be there. In mere hours, they made arrangements and jumped on a plane. It was impulsive, but it was planned. Beautiful! They will remember that forever.

Be impulsive! Savor life. Make memories. But make it planned impulsiveness.

Putting the Pieces Together

What does it mean to win with money? I could ask 20 people and get 20 different answers. We all view it through a different lens. We each possess different skills, and we each have our shortcomings.

What does it mean to win with money? I could ask 20 people and get 20 different answers. We all view it through a different lens. We each possess different skills, and we each have our shortcomings. Some things we'll get right, and other things may be more of a challenge. We don't have to nail every aspect, but it's important to remove any glaring deficiencies. Most families thrive in some areas and struggle in others.

However, I recently met with a couple who inspired me to write about this topic. I've worked with this couple for over a year, but this meeting was particularly inspiring. They are a younger-ish couple, both teachers. In my mind, they've cracked the code on personal finance. No, they aren't geniuses in any one area, but they are doing good in pretty much every area. I'll summarize:

They have unity, a shared vision, and joint ownership of their finances.

They budget intentionally each month, leaning into their unique values.

They have an emergency fund to protect them for WHEN life punches.

They spend money on wants that add value to their life.

They utilize sinking funds to save for future purchases/expenses.

They give joyfully and sacrificially.

They paid off all their non-mortgage debt.

They invest with discipline, simplicity, and effectiveness.

They have cheap term life insurance policies that will replicate each person's respective income in the event of a tragic event.

They are in the process of setting up wills.

They both pursue work that matters, and find meaning and fulfillment in their careers.

They are creating financial margin to provide flexibility for future decisions and lifestyle shifts.

They are the total package! No, it's not because they have massive incomes and unlimited resources. Reminder, they are both teachers. They are normal people, making normal money, living a normal life. Except it's not a normal life. It's an extraordinary life.

What's their secret? Intentionality, discipline, humility, contentment, and consistency. That's it. Good choice after good choice after good choice. Oh yeah, and that whole unity, shared vision, and joint ownership thing. They are doing it together. There is no "mine" and "yours." Everything is "ours." For better or worse.

Yes, this is an opportunity for me to brag about this amazing couple. However, there's more to it. I hope you find encouragement in it. We ALL have the power to get better in the areas of money. The only thing stopping us is us. It's not easy, but it's so, so worth it. Get 1% better today! Then, get 1% better tomorrow. One day at a time. You got this!

“Daddy, When Does the New Month Start?”

I received at least a dozen messages about yesterday's post. Specifically, people were curious how we have open financial conversations with our kids (at age-appropriate levels) while avoiding them feeling the weight of it.

It reminds me of a recent interaction in my house. As I was working on something, Finn approached me with a question. "Daddy, when does the new month start?" "In about a week, bud. Why?" "I want to go to Chuck-E-Cheese to play games. Can we put it in the budget next month?"

I loved his heart in the question. There's something important to him. He recognizes it costs money. He also knows we handle our finances with intentionality. Therefore, he asked if we could prioritize it in the budget.

My response to him? "Of course we can, bud. But we might actually still have money left in the kids category this month. If we do, we should totally go to Chuck-E-Cheese today." I opened the budgeting app and we looked at how much was left. $75! He celebrated wildly, and then a few hours later, we shared laughs over Chuck-E-Cheese games." Side note: Did you know they recently got rid of their creepy animatronic band? I was so mad. Despite being terrifying, that dysfunctional band was a fun remnant of my childhood.

The narrative of our family's money conversations is intentional. We never use the phrase "We can't afford it." Those four words are the ultimate parenting shut-down. It wins the conversation every time. However, it also confuses our kids. For example, if our kid asks for a $30 Lego set and we respond with "We can't afford it," the child may think we literally don't have $30. It also leads them to believe that if we did have $30, we would 100% buy it. It's a weird narrative for kids to wrestle. All the while, we parents are oblivious to how these comments impact them.

Instead, we should talk about money through the lens of intentionality and prioritization. If our kids want something we aren't willing to buy right now, Sarah and I respond that "it's not in the budget this month." We CAN afford it, but it's not part of the plan right now. From there, we can choose not to prioritize it, or discuss adding it to a future budget. Either way, approaching things from the intentionality angle staves off the "I want it now" syndrome.

When we take this approach with our children, they learn the importance of patience, prioritization, planning, delayed gratification, communication, and responsibility. They also learn it's okay to buy fun things. We don't demonize wants. We don't treat fun purchases as wasteful. It's all part of developing a healthy perspective around spending, saving, and giving. Spending on fun things is important.....but it must be done responsibly. Even a seven-year-old can comprehend this if approached well.

Parents, what say you? I'd love to hear your feedback on this topic and any other ideas for engaging in healthy money conversations with your kids.

Smooth Out Your Lumpy Stuff

First, what's the purpose of a sinking fund? A sinking fund is another name for an account funded over time for a specific future expense. These expenses don't happen every month, but you know they will happen at some point. It's not a matter of IF, but WHEN (and how much). I call them "lumpy" expenses.

A few days ago, I wrote about my recent car maintenance frustrations. It was a bit unexpected, but I received a wave of messages from people asking for more insight on how to execute this concept.

First, what's the purpose of a sinking fund? A sinking fund is another name for an account funded over time for a specific future expense. These expenses don't happen every month, but you know they will happen at some point. It's not a matter of IF, but WHEN (and how much). I call them "lumpy" expenses. The goal is to smooth out the lumpy by slowly and steadily funding them over time, eliminating (or significantly reducing) the stress experienced when situations arise. Common sinking fund categories include car, house, travel, medical, giving, and kid activities. Each of these categories has a habit of sneaking up on us. When they do, these sudden and unexpected expenses sabotage our disposable income.....zapping our ability to make progress in other areas.

Here's a step-by-step of the mechanics:

Set up a separate savings/checking account for your desired category and name it accordingly. Most credit unions will let you set up multiple accounts, but most banks won't (with the exception of Wells Fargo). If your bank doesn't, I recommend CapitalOne's 360 Performance Savings.

Allocate money in your budget for this category. The amount can be steady or vary by month, but it must be included in the budget.

Just like you pay your electric bill, you pay your sinking fund. Whatever dollar amount you budget gets transferred to the sinking fund. I prefer to automate these transactions.

When expenses arise for a particular sinking fund category, use your primary checking account to pay the expense.

Immediately after paying for the expense, instruct your sinking fund to send that amount back to your checking account, essentially reimbursing your checking account from the sinking fund.

Repeat.

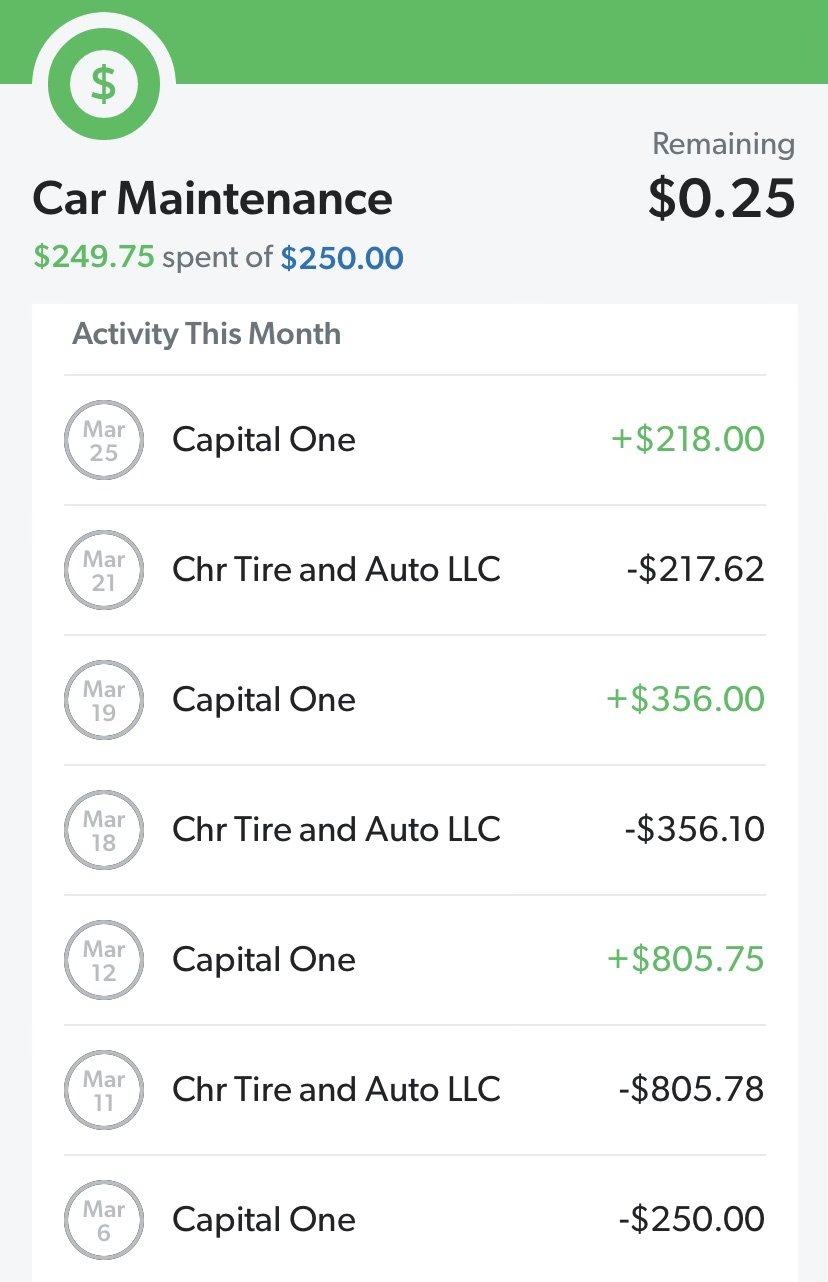

I'll share an example of my car fund from this month. For 19 years, I've budgeted (and automated) a monthly transfer from my primary checking account into my car fund. We currently budget $250/month. After March's $250 contribution (completed on 3/6), our car fund balance was $2,487. Then, we got hit with a hat trick of car bills: $806 for brakes on my main car, $356 for known issues with my new car, and $218 for the unknown issue with my new car. I budgeted $250, but got hit with $1,380 of actual expenses.....ouch! This situation would have crushed our budget had we not had a sinking fund. Instead, I simply reimbursed my checking account from my car fund for each, resulting in a total monthly car fund expense of $250 (the original planned contribution). It took something extremely lumpy and made it smooth. It went from a potential disaster to a minor inconvenience. Below is an image of how we executed it in our budget.

Setting up these extra accounts and steps may appear to make things more complex, but you'll quickly see how truly simplifying (and freeing) it can be! Best of luck smoothing out your lumpy stuff!

Not All Roses and Sunshine

I'm sad to report it's not been all roses and sunshine here in Nissan 350Z-ville. I wish I could tell you I've been happily cruising around in my sweet new (to me) ride for the last few weeks, but that hasn't been the case.

I'm sad to report it's not been all roses and sunshine here in Nissan 350Z-ville. I wish I could tell you I've been happily cruising around in my sweet new (to me) ride for the last few weeks, but that hasn't been the case.

Shortly after bringing the car home from Texas, I took it to my trusted mechanic to address some known issues (and inspect it for the unknown). It was a mixed bag of results, but all was well....or so I thought. I reunited with the car the following day, excited to run my list of errands (top down, of course).

Less than one hour after picking it up, something happened.....and by something, I mean the car wouldn't start. Oh crap! I pulled into the post office to check my PO box. Two minutes later, I couldn't get the car to start. It was dead dead. Crap crap! After some failed troubleshooting, my mechanic hired a tow truck to make the drive of shame to his shop (where it would have to sit over the weekend before getting a formal diagnosis).

Long story short, a little piece of rubber in the clutch wore out. The car is 18 years old, and I suppose that's what happens to things after nearly two decades of life. This little piece of rubber, the size and shape of a Lifesaver, notifies a sensor that the clutch is pressed and it's ok to start the car. When the dumb little Lifesaver broke, my car didn't think I had the clutch engaged. Thus, it wouldn't even turn over.

I'm glad it was a minor issue, but it wasn't cheap. The entire process took six days (it was hard to get a new Lifesaver) and $200 (including the tow). Ouch!

This isn't a sob story—far from it. I'm blessed to have this car, and we sign up for this when we own vehicles. It's not all roses and sunshine. Things happen; life happens. I'm talking about cars, but I'm talking about far more than cars, too. Things happen; life happens.

Since there's nothing we can do to stop life from happening, we have two choices:

Allow life to beat us up, rip us apart, and cause us much stress and turmoil.

Anticipate life happening and be prepared to soften the blow(s).

In the financial world, this looks like sinking funds. I don't know when my car will break, or how much it will cost, but I know it's coming. Therefore, for the last 19 years, I've allocated money in my monthly budget for car repairs. Then, I literally move it to a special savings account for that purpose only. I uncreatively call that account "car fund." Subsequently, when (not if) my car breaks, the money is already set aside to pay for it.

It turned my expensive week from a potential disaster to a minor inconvenience. It's not all roses and sunshine, but it doesn't have to feel like a downpour. What area(s) of your life do you need a sinking fund? They can change everything!

Catch That Breather

Warning: I'm about to share some financial advice that will deeply offend some financial people. If you're still reading this, you've been warned. I take no responsibility for any level of annoyance or disgust you're about to experience.

Warning: I'm about to share some financial advice that will deeply offend some financial people.

If you're still reading this, you've been warned. I take no responsibility for any level of annoyance or disgust you're about to experience.

I recently met with a couple in the middle of a butt-kicking financial journey. They got themselves into a pretty deep hole, and now they're digging out. It's been a slog of an endeavor, but they're making fantastic progress. However, they are flat-out tired. I can see it in their eyes. It's the financial version of seeing a basketball hunched over during a dead ball, clutching his shorts and panting heavily. You can clearly see the tank is empty. They've left everything they had on the court. That's this couple!

Anyway, I could sense they were about ready to break (which is a terrible outcome!). Therefore, I took extreme measures in our last meeting. I encouraged them to stop paying debt next month. Yes, completely stop. No debt payoffs, no saving, no investing.....nothing "responsible." Instead, aside from their needs, minimum debt payments, and giving, they will use ALL of their extra income for "irresponsible" things. Dining out, travel, personal spending, and maybe a few fun things for their house. Totally irresponsible!

Three powerful things will happen when they follow through with this ridiculous-sounding plan:

They will get a much-needed break. They are exhausted, and this one-month progress break will be the equivalent of a coach giving their star player a short breather. This break will give them the energy to get back on the court and finish the game strong.

They will experience first-hand that it was not wants that hurt them in the past, but a lack of intentionality. On the flip side, when they experience a month chock-full of fun want spending while simultaneously keeping the financial train on track, it will show them that wants aren't the problem. It's all about intentionality. This experience will change them!

These things won't inherently make them happy. They will be fun, but they won't move the satisfaction needle as much as those progress months do. This will further embolden them to get back on the court and take care of business once and for all.

"Irresponsible" spending only. No progress. No wise moves. No debt payoffs. No saving. No investing. Just fun things. Just because. This is the break they need. This is just what the doctor ordered to propel them to that next level.

If you can relate to this couple, perhaps you need a break. Maybe you need to catch that breather. It's ok if you do. Even Jordan needed one every now and then.