The Daily Meaning

Take your mornings to the next level with a daily dose of perspective and encouragement to start your day off right. Sign-up for a free, short-form blog delivered to your inbox each morning, 7 days per week. Some days we talk about money, but usually not. We believe you’ll take away something valuable to help you on your journey. Sign up to join the hundreds of people who read Travis’s blog each morning.

Archive

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- August 2021

- November 2020

- July 2020

- June 2020

- April 2020

- March 2020

- February 2020

- October 2019

- September 2019

Chicken or Egg?

I recently stumbled upon a heated online conversation on a social media platform. The original poster posed a question: "If so many people are struggling right now, why are there so many people with brand-new vehicles parked in their driveways?"

I recently stumbled upon a heated online conversation on a social media platform. The original poster posed a question: "If so many people are struggling right now, why are there so many people with brand-new vehicles parked in their driveways?" It seemed counterintuitive, as these new vehicles are presumably evidence that people are doing well.

Let's just say the comments were lively. Hundreds of people chimed in, positively confirming that most people are, in fact, doing great. The commenters believed they, individually, were simply part of the small share of people who are struggling, while everyone else is thriving.

I have news to break to them (and anyone else who will listen). Those brand-new vehicles sitting in people's driveways aren't evidence that people are doing great. Rather, those same vehicles are one of the primary culprits for why people are struggling so much. People's vehicles are putting them into a financial grave, month after month.

I recently met with a successful-looking couple who, from the outside, appear to have it all put together. They are fit, their kids are cute, their house is immaculate, they have good jobs, and they both drive new vehicles. The subject of the conversation? How they can stay financially afloat and not lose everything. Truth be told, their monthly finances didn't contain many red flags. Lots of normal, but not outlandish spending allocations. However, there were two major red flags.....and both were parked in their garage:

His vehicle: $1,100/month payment

Her vehicle: $850/month payment

Total vehicle payments of $1,950. In my brain, that's called a mortgage payment. Two thousand bucks for vehicles!?!? Both assured me that 1) they can afford them, 2) they are perfectly reasonable vehicles, and 3) everyone else has at least as nice vehicles as they do.

They aren't alone. This is a dynamic I see every single week in my coaching work. I've met with hundreds of families, and vehicle tension is the leading contributor to financial pain, suffering, tension, stress, and destruction. Not a lack of income, student loan debt, a failure to budget, or limited financial literacy. Vehicles. Vehicles are literally milking an entire society dry.

Many people who read this piece will roll their eyes at me. This topic often draws the ire of those who digest my content daily. That's okay, though, as this message needs to be shared over and over and over. I so badly want people to live a quality of life, and if I can get them to make different decisions in this vehicle department, I strongly believe it will have a direct positive impact on their quality of life.

We need more humility. We need more patience. We need to care a whole lot less about what others think. That's the ticket to some beautiful things in our lives. Please don't allow a vehicle to play a significant role in your journey. It can play a role, but not a leading role. You deserve better; much, much better!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

What’s Your Weird?

People frequently tell me that I'm "weird" in how I spend money.

People frequently tell me that I'm "weird" in how I spend money. I never take offense to these comments. In fact, I love them! I wear them as a badge of honor, and in some ways, they tell me I'm right where I need to be. Here are some examples of things people have told me I'm weird for doing:

When it comes to my personal residence, I'm a perpetual renter. I've owned two houses in my adult life, but I much prefer renting over owning.

The biggest category in our household budget is giving. This is non-negotiable.

Our second-largest category is travel. This is also a non-negotiable.

I will gleefully spend a few hundred dollars on a first-class meal. I've had $25 dinners that felt expensive and $250 dinners that felt cheap. An amazing meal is worth its weight in gold.

There's no amount of money too much when it comes to creating once-in-a-lifetime memories.

When I'm at a coffee shop, restaurant, or bar with someone, I almost always offer to pay for them.

If someone offers to buy my coffee, meal, or drink, I accept.....always. No exceptions.

When eating at a sit-down restaurant, the minimum I’ll tip is 20%, but it’s usually closer to 40%-50% if the server demonstrates excellence. It’s one of the few areas of life where people will gratefully accept generosity, so I love to lean into it as much as possible.

I will never purchase a new vehicle. In fact, I've never purchased a new vehicle. At best, any vehicle I purchase is probably at least 3-4 years old.

I will always pay for services that save me time, sanity, or stress.

What say you? Do you find these weird? I hope so, as you're different than me. That's what makes this money stuff so fascinating. We're all wired differently, heavily influenced by our experiences, values, upbringing, and circumstances.

I want to know what weird money habits you have. Please hit reply to this e-mail if you're a subscriber, or comment below if you're on the website. Please share your quirks with me. If enough people reply, I'll put together a fun little list and share it in a future post. Have an awesome (and weird!) day.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

The Want-to-Need Migration

Much discourse centers around the idea that life is so much more expensive today than it used to be. We blame inflation, capitalism, Boomers, politicians, and the systemic structure of our modern-day society.

Much discourse centers around the idea that life is so much more expensive today than it used to be. We blame inflation, capitalism, Boomers, politicians, and the systemic structure of our modern-day society. In other words, we love to blame everyone except the person in the mirror. Has life gotten more expensive? Sure. It always does. That's how inflation and the time value of money work. In all of this discourse, I think we've missed the biggest culprit of all: the want-to-need migration.

Over the past 25 years, I've personally witnessed a slow and steady cultural shift from what was once a want to now a need. Houses are a great example. When I was a kid, young families lived in small, conservative houses. However, over time, the average square footage of houses in America grew, as did the expectations of younger homeowners. Houses we now consider "starter homes" would have been mini-mansions 25 years ago. What about those small, conservative houses people used to live in? It would be unthinkable to live there!!!! Out of the question! Our expectations for the houses we choose have migrated from a want to a need.

Dining out is another great example. I recently met with a family who said a $600/month dining out budget is a "need." They didn't want a $600 dining out budget; it was a basic human need for their survival. Conversely, 30 years ago, dining out was more of a luxury. In my house, it felt more like a twice-per-month event. Taco Bell was a treat, Pizza Hut was a splurge, and Golden Corral was fancy. Our dining out habits have migrated from a want to a need.

Off the top of my head, I can think of countless items we now call needs that would have been wants 20+ years ago, including:

Streaming services (many people didn't even have basic cable in the 80s and 90s).

Cell phones (not in most people's budgets).

Internet service (also scarce).

Plane tickets (air travel used to be rare; today it's the norm).

Coffee shops (as the 90s kids ask, "What's a coffee shop and why would anyone go there?")

Online shopping (it was much harder to spend money in the pre-internet days, when you used to have to drive to the store. Today, click, click, click....delivery in an hour).

I'm not saying there's anything wrong here. In fact, I enjoy all of those things I just listed. They are part of my budget and part of my family's rhythm of life. I'm grateful for them. However, we ought not forget what's really a need and what's really a want. Sometimes, we need to get back to basics: food, clothing, transportation, and shelter. Let our needs be needs, then address our needs head-on. Once we've accomplished that, then we can move on to the wants. But let's let wants be wants. View them as such. Treat them as such. Enjoy them as such. Don't let your wants migrate into needs.....that's the gateway drug to much stress and bad outcomes.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

If Everything Is Important…..

Here's a general truth. If everything is important, nothing is important.

I received a half-dozen messages yesterday in defense of the family I discussed in yesterday’s post. In short, people defended this family's actions by saying that all of these things were important. Thus, this family was simply a victim of having all these important things stacked on them.

Here's a general truth. If everything is important, nothing is important. Let's say there are 50 different things vying for our time or money, and all of them are deemed "important." If they all occupy the same plane of importance, then none of them are actually important. In a world of relativity, none of them win.

This is the curse that strikes so many of us. Our budgets are living testimonies of this. For example, I'll regularly meet people who are actively saving for 15 different things—$ 25 here, $30 there. When I do the math, I point out to them that it will take years to knock out any of them. That becomes immensely frustrating, eventually defeating.

For this reason, we need to truly prioritize. Are some of these things in our lives needs and wants? Yes. That's totally cool. Allow them to live in our hearts and minds. However, we need to be honest with ourselves when setting priorities. Once we have our list of upcoming needs and wants, do whatever it takes to prioritize them so your values can be lived out.

If everything is important, nothing is important. Therefore, keep it simple, prioritize, and execute. Confidently knock out the most important goal, then move on to the next.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

There’s Always Something

Here's another problem: this is only the most recent in a string of unexpected needs. Truth be told, they've been putting off this big, important dream for more than six years! Why? There's always something!

A couple I know has some big aspirations. Their values and goals are clear, and they know what it will take to achieve them financially. One problem: something came up. An unexpected need arose, and they must delay this goal until they address it.

Here's another problem: this is only the most recent in a string of unexpected needs. Truth be told, they've been putting off this big, important dream for more than six years! Why? There's always something!

I'll illustrate for you.

First, they decided that buying a new vehicle was an immediate need. $27,000 of saving, 15 months of time, and another $35,000 of vehicle debt later, they had their new vehicle and were ready to achieve their dream.

Second, they decided that buying a house was an immediate need. $20,000 of saving and 12 months of time later, they had their house and were ready to achieve their dream.

Third, they decided that a dream Disney vacation was an immediate need. $18,000 of saving and 11 months of time later, they took their trip and were ready to achieve their dream.

Fourth, they decided that finishing their basement was an immediate need. $40,000 of saving and 18 months of time later, they had their new basement and were ready to achieve their dream.

Fifth, they decided that buying the other spouse a new vehicle is an immediate need. They are currently saving for this. But once they have this new vehicle, they will be ready to achieve their dream......

There's always something! When asked why they haven't pursued their huge dream yet, they will cite not being able to afford it. But when you look at the items above and how many resources they put toward them, it's easy to see that they could have done some amazing things over these past six years......they just chose to do something else instead.

Just remember, there's always something. Some things are in our control, and some aren't. However, far more is in our control than we'd like to believe. Please don't allow yourself to be a victim of your own life. Seize control of these decisions and prioritize your time, resources, and actions in accordance with your true values. Future you deserves it.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Don’t Let the Sequence Fool You

This young guy fell into the same trap so many do. Instead of viewing his money as a giant puzzle, he viewed it as a sequence of transactions.

A young man asked me to look over his finances and help him get some control. Included in this conversation was a review of his most recent bank statement.

"Dude, you spent $700 more than you made last month!" I exclaimed.

"I had to buy groceries at the end of the month. What, you expect me just not to eat?"

"No, I expect you not to implode your finances by plunging yourself into debt."

"I had no choice, Travis! Either I buy groceries, or I don't eat."

"The sequence of your purchases isn't what matters here. That $700 of overspend doesn't just get credited to the last $700 you spent in the month."

"Again, I HAD to buy groceries."

"Did you need the other $1,200 of impulse purchases you made before that?"

“……….”

This young guy fell into the same trap so many do. Instead of viewing his money as a giant puzzle, he viewed it as a sequence of transactions. Then, when he had known and tangible needs, he acted (even though he had already exceeded his budgeted income for the month). This is how we end up in debt. This is how we never have funds for wants. This is how we can't afford to invest. This is how we justify not giving. We spend, spend, spend, then when a NEED arises, we flippantly meet that need without regard for the consequences.

It's a psychological phenomenon that often strikes us humans. If you're human, you're subject to it. What's the solution? Have a plan for the month. The WHOLE month. We know we need groceries. We know the rent or mortgage has to get paid. We know we'll need to put fuel in the vehicles. These are known expenses. Therefore, plan accordingly. While we're planning, we should also plan for the fun stuff. Plan for the dining out. Plan for the date nights. Plan for the concerts. Plan for the plane tickets. Plan for the new clothing. The keyword is "plan."

Let's remove the bias toward sequence and replace it with a bias toward intentionality. Oh, you really, really want a new Blackstone grill? Great! Is it in your plan? If not, then don't do it. Put it in your plan next month. Then buy it! The goal here isn't to demonize spending, but to demonize unplanned, impulsive, destructive spending. Let your plan be your plan, then execute. If it includes a fun trip or a Blackstone grill, go for it! But we can't constantly buy things that aren't in the plan, blow past our budget on buying true needs, then blame the needs.

We can do better! We deserve better. We'll thank ourselves for giving ourselves better!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

To Save a Few Bucks

In my 20s and well into my 30s, I followed a certain practice. It was a practice instilled in me from a young age and affirmed at every step through adulthood. The practice? DIY projects. Trouble with a toilet....figure it out. A landscape project needs to be installed.....figure it out. A large and complex piece of furniture needs to be assembled.....figure it out. If we can save money by figuring it out ourselves, that's a win! After all, that's what men do!!!!!!

Then, in my mid-30s, I finally broke. Sarah and I moved into our new house, and I needed to mount a TV above the fireplace. I bought the parts, collected the tools, and watched the appropriate YouTube videos to teach me everything I needed to know about mounting a TV above a fireplace. Six hours later, I had a damaged TV, a damaged house, and still no TV mounted on the wall. I tried to save a few bucks, and all it got me was a boatload of stress, a wasted Saturday, and a higher financial cost from the damage I caused than it would have cost me to just have a pro quickly knock it out for me. That's what happens when pride gets in the way. Pride and, well, irrational frugality. I was acting too cheap to make wise choices, and we paid the price for it.

Fast forward into the back half of my 30s and now well into my 40s, and I've turned over a new leaf. I will always opt to invest money in a pro to help me out. Sure, it costs some money. However, it saves time, stress, and the risk that I'll do far more harm than good. That, in my book, is a wise investment!

We can save a few bucks if we want. That option is certainly on the table. However, it's not the only option. Never be afraid to hire out tasks that will save your stress, your time, and ultimately, even more money than it costs. We should never overlook the value of our time and our sanity. Money may have a nominal dollar value tied to it, but our precious time and mental health are priceless.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Blind Spots: Pet Edition

In my 10+ years of coaching, though, I've realized that pets are one of the biggest financial blind spots for families.

I love dogs. I grew up with a dog and never pass up an opportunity to pet a random dog on the street. If the boys keep asking hard enough, we might actually get one for our household soon, too.

Buddy, my childhood friend, showing off part of his Michael Jordan jersey collection.

In my 10+ years of coaching, though, I've realized that pets are one of the biggest financial blind spots for families. It never fails. When I'm going through the initial budget with a new client, and we get to the pet category, the answer is always some form of, "Oh, we spend almost nothing on pets. Probably just a $50 bag of food every few months."

That's when my eyes get really, really big. Pet expenses are secretly crushing people's finances from right under their noses. Yeah, that bag of dog food might only cost $50, but all the other things we don't think about cost hundreds.....or thousands. And the vet expenses!!!! Here's what a typical vet expense monthly rhythm looks like: $0, $0, $0, $0, oh crap! That "oh crap!" moment is where the wheels fall off, and where the math works against us. Pets get sick. Pets get hurt. Pets make poor choices.

I didn't want this piece to be merely anecdotal, so I dug into my client files to find some real-world data. I looked up 8 active clients who have 2+ years of pet data. Here's what it looks like (in order of my research discovery):

$9,130 over 51 months = $179/month

$5,860 over 21 months = $279/month

$6,815 over 47 months = $145/month

$5,850 over 45 months = $130/month

$11,730 over 24 months = $489/month

$15,744 over 24 months = $656/month

$4,320 over 36 months = $120/month

$16,482 over 41 months = $402/month

In total, these eight randomized clients had an average monthly pet spend of just over $260/month. I don't know about you, but that's a tad bit different than a $50 bag of food every other month. These families range anywhere from $120/month to $656/month, with unexpected vet bills being the key driver of how high this category can get.

Pets are also one of the main culprits of credit card debt, as there's a deeply emotional component to this. When faced with a life-or-death decision regarding our beloved pets, it's hard to emotionally look ourselves in the mirror and put a rational price tag on our go/no-go decision. Thus, we simply act now and sort it out later. This is having some pretty harsh consequences for families.

Again, this isn't an indictment of pets or pet ownership. Rather, this is my encouragement to make decisions with our eyes wide open. It's totally okay to financially prioritize pets, but we ought to understand what we're really getting into from a financial perspective. The same goes for other categories, too! Eyes wide open is always the best approach. That way, our cute little pets (and all the other choices we make) can truly be blessings in our lives, and not pain points.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Define “Actually Enjoy Life”

What if enjoying life is so much more than how much we can spend and how little we can work?

I received split feedback about the recent post titled A Middle Finger to Our Future Selves. Specifically, it was about the following excerpt:

"...the idea that we don't know whether we'll even be alive when we're older, so we might as well "enjoy life" while we're young. And by "enjoy life," he meant spend, spend, spend. He hated the idea of saving, or heaven forbid, investing. If he had it, he was going to blow it on something fun."

One blog reader replied to this post and said the following: "Your friend is right you know. We should actually enjoy life while we're young and healthy."

I think this comment gets to the heart of a really important decision. How do we define "actually enjoy life"? The friend in my previous post, this blog reader, and countless others tend to define "actually enjoy life" as some combination of spending money on wants and not working. Those seem to be our two cultural measuring sticks of "actually enjoying life."

What if enjoying life is so much more than how much we can spend and how little we can work? I tend to look at life through the lens of meaning. Am I living my most meaningful life? If the answer is yes, then there's a strong probability that I'm "actually enjoying life." If the answer is no, then I may have some issues. But how much money I can spend on wants is not a real driver in that discussion.

This is why contentment is so important. If we define our enjoyment by how much money we can spend on wants, then our ability to enjoy life is essentially capped by our income and resources. If we have many resources, we can be happy. If we don't, we can't. That's a really depressing proposition. Fortunately, it's a lie.

Contentment, on the other hand, disconnects the two altogether. The people I know who are the most content live tremendously enjoyable lives despite having limited resources. They don't allow stuff and leisure to define happiness. This disconnect in definitions is also one of the reasons there are so many people unhappy, fantasizing about retirement, while others are still working in their 70s, happy as a clam. This group of positive and optimistic people aren't defining themselves by how much they can spend or how little they can work. They are merely soaking up every bit of meaning they can find in this life.

Yes, we should "actually enjoy life." Amen to that! However, I don't think it's as simple as deciding to spend as much money on wants as possible. Instead, I believe it comes from pursuing meaning each and every day. Meaning in our home life. Meaning in our work life. Meaning in our generosity. Meaning.....period. The rest will sort itself out.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

What Is a Memory Worth?

For the past 25 years, I promised myself that if I ever had a chance to attend a World Cup game, I would.

For the past 25 years, I promised myself that if I ever had a chance to attend a World Cup game, I would. Well, we are nearing the fulfillment of my wish and a referendum on my promise to myself. The World Cup is hitting the U.S. this summer, and one of the host cities is three hours from my house (and 30 minutes from my sister-in-law's). Will I do it? Will I follow through on the dream of younger me? We shall see.

Looking at the calendar, I have the opportunity to watch two teams I have no affinity for or allegiance toward. But it's the freaking World Cup!!!! The get-in price is currently $313 per person. That's the worst seat in the stadium.....for $313.

But what is a memory worth? No matter what happens or how the game goes, going to that game will be a lifelong memory. No question about that. Therefore, if this is something I'll remember for my entire life, is it worth at least $313? I think that's a resounding yes.

Will I actually do it? Only time will tell. Perhaps that's one of the reasons I'm writing this post: So hundreds of people will hold me accountable to my own principles!

I think it's an interesting idea, though. It's so easy to get hung up on prices for things that, on the surface, should cost far less than they do. We look at these prospective transactions and try to view them objectively. We put our logical caps on and attempt to do a little cost-benefit analysis in our heads. Ultimately, though, we sometimes have to throw out the normal playbook and understand we're talking about a lifelong memory. That, in my opinion, can trump the normal decision-making process.

What about you? What's something that might not make much sense on paper, but in the long run, you believe is a steal of a deal, no-brainer?

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Throwing In the Towel

Have you ever experienced retail rewards anxiety? You walk into a shop and either a) forget to scan your rewards, or b) can't get it to work. There's this weird anxiety-mixed-with-guilt-mixed-with-regret feeling that seeps in.

I stopped to get gas for my car the other day. The fuel pump asked me to enter my rewards number.

I purchased a cartful of groceries. The cashier asked me if I had rewards.

I bought a Cruchwrap Supreme at Taco Bell. The kiosk asked me to check in with my rewards account.

I stopped at a local coffee shop. The barista asked me if I had a rewards punch card.

I'm tired, guys! I can't keep up with this. I want to keep up with it, but at the same time, I can't. It took nearly 45 years, but I decided yesterday to draw a line in the sand. Regardless of whatever rewards I could be earning, I need to completely turn my back on rewards programs. Ultimately, the upside doesn't even come close to the mental and emotional fatigue it costs to manage all of this.

Have you ever experienced retail rewards anxiety? You walk into a shop and either a) forget to scan your rewards, or b) can't get it to work. There's this weird anxiety-mixed-with-guilt-mixed-with-regret feeling that seeps in.

Starting today, I am experimenting with ZERO rewards. I'll buy what I buy, then I'll move on with life. Whatever I pay in lost rewards, I will surely make up for in saved stress, emotional energy, guilt, regret, and time managing it all.

Want to guess how many apps I just deleted off my phone that are correlated with rewards programs? Seven. Just in apps alone, I deleted seven different store-specific reward apps. No gas stations. No restaurants. No grocery stores. No anything!

I haven't even visited a store since I made this decision, and I already feel 25 pounds lighter. Reward programs are specifically engineered to lure us in, entice us, and modify our behaviors. I've always been leery of falling too deeply into them, but today, I'm fully throwing in the towel. I'm untethered from outside influences and shiny little carrots hanging above my head

Where do you stand on this subject? Are you an avid reward user? Do you turn your back on them? I'm curious to hear where this lands with people. I'm excited for this little experiment, and I'll be sure to report back soon.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

What Else Are We Supposed to Do?!?!

A friend of a friend recently made an exciting decision: He purchased a new car!!! Everyone around him is so excited. "Congratulations!" exclaimed one person on social media. "Well deserved," quipped another. Silently, I mourned for him. He did exactly what he was supposed to do, and now, he's screwed.

A friend of a friend recently made an exciting decision: He purchased a new car!!! Everyone around him is so excited. "Congratulations!" exclaimed one person on social media. "Well deserved," quipped another. Silently, I mourned for him. He did exactly what he was supposed to do, and now, he's screwed.

He's a young man in his early 20s, with an okay job ($22/hour, full-time). It's not a bad job, but after I tell you the next part, you'll probably cringe. He has a $62,000 loan on his new purchase. I don't know the exact terms of his financing, but it's highly likely that his monthly payment is north of $1,000.

When I asked my friend about this guy's decision, he said something interesting. This young guy was just trying to do what he's supposed to do. He needed a car, new cars cost a lot of money, so he did what he needed to do to buy it. It's not his fault that he doesn't have a higher income. It's not his fault that cars cost so much. It's not his fault that his new payment is going to crush him. This is the way of the world, and he's just trying to survive.

This young man isn't alone. In fact, I'd say more people fall into this line of thinking than not. It's pervasive.....and it's destructive! I regularly meet with folks who are burdened by crushing vehicle loans. Very rarely do they admit there was a mistake made. Instead, they typically do what this young man did: defend it through the lens of what culture says we should do, have to do.

Is there an alternative? Of course there is! Sarah and I haven't had a car loan for the entirety of our 17-year marriage. It's not because we've always had so much money. Rather, it's because we said we would never again have car debt, then made decisions to honor that promise. What does that look like? In our case, only buying vehicles we could afford. I've never paid more than $19,000 for a vehicle, EVER. Here, I'll show you:

Age 16: $7,000 (if I remember correctly) - used debt

Age 17: $2,500 (after totaling above vehicle) - with cash

Age 19: $19,000 (stupid!) - with a LOT of debt (stupid, stupid!!!)

Age 26: $10,000 (reasonable) - with cash

Age 30: $15,000 (car for me) - with cash

Age 35: $18,000 (car for Sarah to fit twin babies) - with cash

Age 36: $16,000 (replacing a car that got totaled) - with cash

Age 42: $9,000 (my fun 350z convertible) - with cash

We'll soon replace Sarah's vehicle that we purchased a decade ago for $18,000, which now has about 250,000 miles. The budget is $25,000 for a used Toyota Sienna. Why used? Because that's the amount we can justifiably afford without going into debt. It's not easy, but it's simple.

At the exact same time, young adults all over America who are making a much lower income than us are spiraling into crippling debt because "that's what we're supposed to do." Please don't fall for the trap. It's not worth it. I promise, it's not worth it!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Alternatives

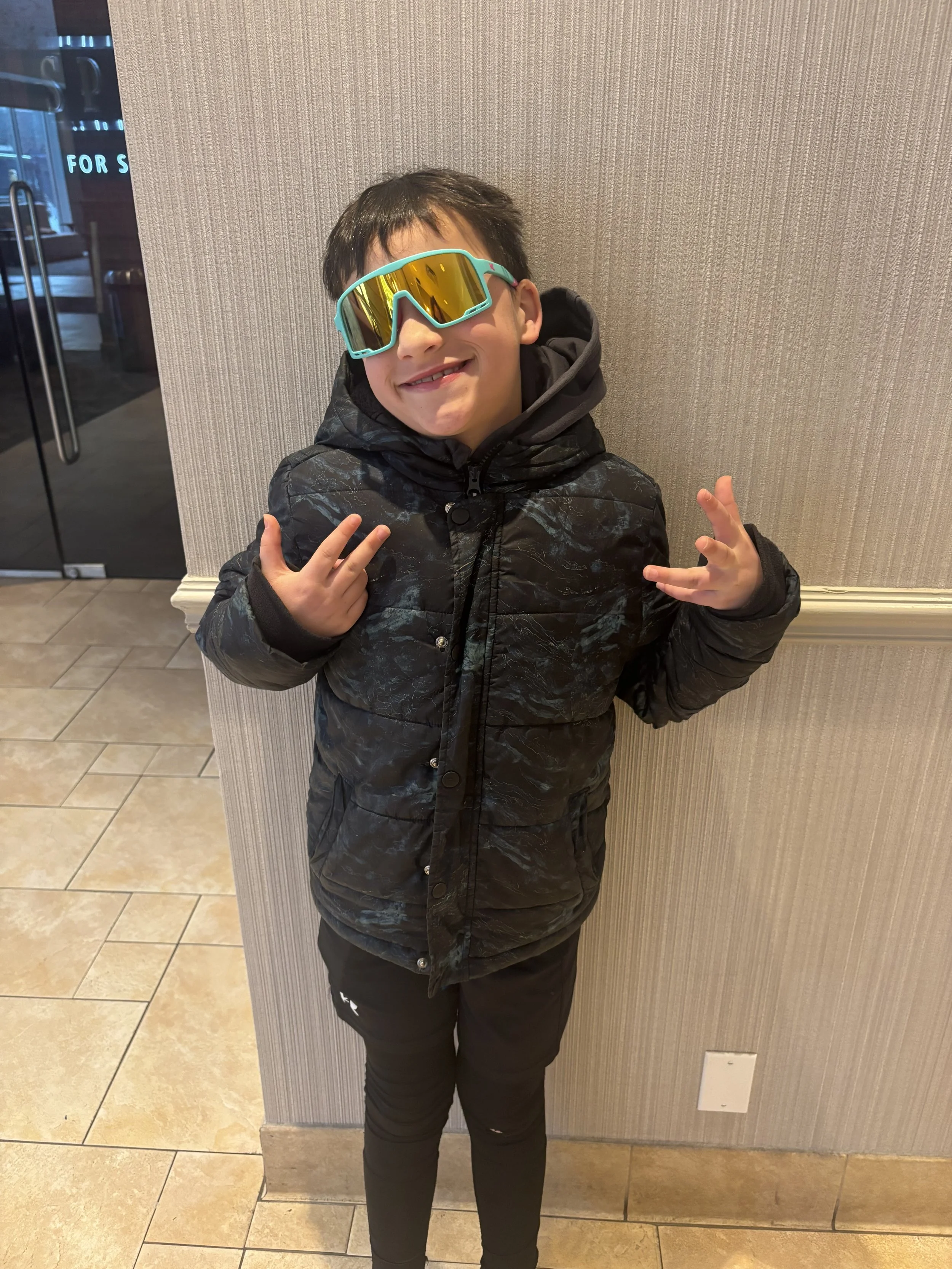

My son Pax has been dead set on buying a pair of $125 Oakley sunglasses.

My son Pax has been dead set on buying a pair of $125 Oakley sunglasses. I've been careful not to poop on his aspirations, but I've secretly been hoping he would eventually change his mind. $125 for a pair of sunglasses is a lot for an adult, never mind a third grader. The good news is that it takes a 9-year-old a long time to save up $125. As of this weekend, he was sitting on about $102.....close but not close enough.

Without explicitly saying it, I think he's been feeling the weight of this prospective purchase. He's experiencing just how much work is involved in saving for a single pair of $125 sunglasses. Then, yesterday happened. As we walked through Dick's Sporting Goods, he caught sight of a cool pair of sunglasses. He beelined it to the display and hurried to try on a few pairs.

Just a few minutes later, he decided to pull the trigger. $45. Just like that, he had an awesome pair of sunglasses he loved, plus $57 of cash leftover from his sunglasses fund. He found the perfect alternative, and it beautifully propelled him forward.

Not the style I would have chosen, but he loves them!

This is such an important topic for each of us to confront. Often, we get locked into a particular plan. We concede that something will cost a certain amount of money, time, energy, or sacrifice. For whatever reason, we develop tunnel vision and build our reality around this way being the absolute unyielding truth.

What are the alternatives, though? I recently met with a couple who are having brutal car issues. Their current vehicle is starting to absorb large chunks of repair money. What should they do? In their minds, there is only one option: purchase a new vehicle, which will cost between $55,000-$65,000. That's it. That's their fate.

What about alternatives? There are no alternatives, they exclaimed! Continue eating big repair bills, or buy a new car. In their situation, said new car would require a huge loan with a huge monthly payment. Oh well, they thought, it's their new reality. Tunnel vision set in.

It took a few conversations, but fortunately, they started to see some alternatives taking shape. After a few months had passed, they elected to purchase a reliable used vehicle that a) eliminates the repair issues they were dealing with, and b) avoids the painful cost of the debt that a new vehicle would surely create. They had the same look on their faces as Pax had yesterday when he purchased his alternative sunglasses: Relief, contentment, and peace.

Life is filled with alternatives.....if we're willing to look. When I look back at my adult life, some of the best purchases and decisions I've made were actually alternatives to the primary plan I set for myself. Whether knowingly or unknowingly, my eyes were opened to a better, more effective alternative. Each time that happens, I could feel my life propel forward. Relief, contentment, peace.

Always look for the alternatives.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

You Don’t Have to Play Their Game

A jacked dude is sitting in his car, saucing up the fat burrito he just purchased. As he's preparing to take his first bite, he's complaining about how it's absurd that two burritos cost $37.

One of my favorite subgenres on social media is the one where people whine and cry about how much businesses rip them off. Chipotle is probably my favorite. A jacked dude is sitting in his car, saucing up the fat burrito he just purchased. As he's preparing to take his first bite, he's complaining about how it's absurd that two burritos cost $37. Chipotle never used to cost this much, he exclaims. It's highway robbery! He takes a giant bite into his juicy burrito, then complains some more.

Chipotle, Five Guys, Disney World, new cars, airport restaurants, drinks in clubs, Ticketmaster, etc. There's no end to the complaining people do for decisions they voluntarily and willingly make.

One of my friends was recently lamenting the fees charged by Ticketmaster. He goes on and on and on about it. "Did you enjoy the show?" I asked. "Yeah, it was amazing!!!" "Would you do it again?" "Yeah, in a heartbeat." So, what's the problem?

Here's a little encouragement. You don't have to play their game. If you don't like the price of Chipotle, don't go. Simple as that. If it's really that big of a ripoff, then don't go. Go to one of the hundreds of dining alternatives. But if you're still going to go, own it. If you're willingly going to pay $18 for a fast-food burrito, embrace it. Enjoy it; savor it. Don't whine about it.

This is a wild part of behavioral science that I'm increasingly fascinated by. In a world where we have near-unlimited choices, we're intentionally (and repeatedly) choosing to go to XYZ businesses, then continuously whining about how big a ripoff they are. It's bonkers!

You don't have to play their game. If I think somewhere is a ripoff, I don't go. If I think something is a ripoff, I don't buy it. In the event I do willingly purchase something that's questionably a ripoff, I own it. I made that choice. There was no gun to my head. We look awfully ridiculous when we make a choice to do something, then become a victim of said choice.

If you want to slam that burrito, slam that burrito. If you want to avoid that place, avoid that place. In the words of a wise mentor, "Let your yes be yes, and your no be no."

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Ridiculous or Not

One of my friends caught wind of something "ridiculous" my wife spent money on. I'm not sure whether he heard it from his wife or from me, but he's right: Sarah's purchase did fall into my definition of "ridiculous." "Why would you let her spend money on x thing that you don't even agree with? I would have just said no."

One of my friends caught wind of something "ridiculous" my wife spent money on. I'm not sure whether he heard it from his wife or from me, but he's right: Sarah's purchase did fall into my definition of "ridiculous."

"Why would you let her spend money on x thing that you don't even agree with? I would have just said no."

Are any spouses seething yet? Good, let the anger soak in for a moment.

Here was my two-fold response:

First, I don't "let" her do anything. Our financial decisions are joint, and she has just as much say as I do. I don't give her an allowance like a child. She negotiates for what she believes is important when we construct our monthly budget.

Which brings me to my second point. If it's important to her, it's important to me......period. Even if I think something is ridiculous (and I often do with Sarah!), that doesn't matter. If it moves the needle for her, I must support her in that. Therefore, when it's important to her, it's important to me. Something fun happens when we take that posture: It gets reciprocated. I promise I spend money on things that Sarah thinks are absolutely ridiculous, too. But just like me, she supports my ridiculousness because it's important to me.

Yes, we should have financial unity in marriage. I'll 100% die on that hill. It's critical to a successful marriage and to successful household finances. That doesn't mean both spouses will value every expenditure equally. Some expenditures will be more your thing, and others will be more your partner's thing. That's okay! That's what makes you a team, and that's what it looks like to sacrifice for each other.

So, yes, I suspect Sarah will continue to desire "ridiculous" purchases. I'll support her every step of the way. If it's important to her, it's important to me.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Yeah, Definitely Didn't "Need" This

Seeing the joy and wonder on my son's face, followed by the endless conversation and dreaming about what we can design and build together, is further affirmation that this financial expenditure will add so much value to our lives.

I have twin nine-year-old sons. One of them is a miniature version of me. We have a 99% overlap in interests, and as such, we naturally bond over these similarities. My other son? Well, if I'm being honest, we probably only have a 10% overlap in interests. He couldn't be more different from me, which can make bonding difficult at times. I love that little man to death, but we don't naturally gravitate toward each other.

________________

In a talk I gave earlier this week, I attempted to debunk the cultural myth that we shouldn't spend money on things "we don't need." It's a pervasive narrative hovering over us, causing shame, guilt, regret, and anxiety whenever we buy things that are simply wants. In other words, it sucks some of the joy out of life. I personally believe that spending some of our resources on wants is a critical part of the journey in creating a healthy relationship with money. Yes, we need to take care of our needs. Yes, we need to save. Yes, we need to give. Yes, we need to invest. But we also need to spend money on things that add value to our lives.

The truth is, I don't spend much of my personal spending money each month. A few books here, a couple coffees there, and maybe a few lunches with friends. However, in the spirit of making sure I don't become a hoarder incapable of spending on wants, I often bank mine for a period of time before purchasing a larger item.

Yesterday was my day! In an effort to find new ways to bond with my son while simultaneously utilizing my saved-up personal spending money, I purchased a 3D printer. $850! The kids' heads practically exploded when we picked it up from the store. I'll go out on a limb and say there's no "need" for an $850 3D printer…..or any 3D printer for that matter. However, that's what makes this money journey so much fun. It's not about need or not a need. It's about adding value to our lives, keeping everything in context with the broader plan.

Seeing the joy and wonder on my son's face, followed by the endless conversation and dreaming about what we can design and build together, is further affirmation that this financial expenditure will add so much value to our lives. I'm grateful for the opportunity to purchase this "want," and I look forward to much bonding time with my little guy.

Buck the myth. It's not irresponsible to spend money on things you don't need. Don't fall for the lie. Don't let shame, guilt, regret, and anxiety take hold of you. We can't have all the wants, but we can have some. Make sure your some includes things that truly add value to your life.

Now, if you'll excuse me, I have a life-size Lego head to print.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

The Value of a Pizza

Was the local pizza 4-5x better than a frozen pizza? Was the local pizza 2.5x better than the national chain pizza? Probably not.

"Dad, can we have pizza tonight?"

Ah, the common words of a nine-year-old. The boys were craving pizza last night. Since I, too, was kinda craving pizza, I wasn't about to fight the idea. "What should we get?" I asked.

Lots of ideas were tossed around, ranging from frozen pizza, to national chain to-go pizza, to local pizza shops. Ultimately, we (unsurprisingly) landed on our favorite local pizza shop. Additionally, there was one more request: "No pick-up. Let's eat there." Deal!

Pizza is one of those things that has a wide range of styles, quality, and prices. For example, we could have gotten a decent frozen pizza for $5-$7 or grabbed a national chain pizza for $10-$12. Instead, we paid $20 (plus tip) for a pizza....around $26 total. Was the local pizza 4-5x better than a frozen pizza? Was the local pizza 2.5x better than the national chain pizza? Probably not. It's pretty good pizza, don't get me wrong! We love this pizza. But 2.5-5x better than the alternatives? Not exactly.

It's not really about the pizza, though. Sure, we were there to eat a pizza. However, what we were really there for was an experience. We wanted to go to our spot, enjoy our time together, engage with the familiar staff, and create memories. We didn't pay $25 for a pizza......we paid $25 for an experience that happened to include a pizza.

We had a blast. We talked about all the fun things we did earlier in the day, and looked forward to the week ahead. It was a good time. The pizza was fantastic as well, but that wasn't the heart of the story.

Memories, experiences, adventure, and time with those we care most about. That's always worth investing in.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Managing the Puzzle Pieces

Sarah must have picked up on my lack of a good poker face. Translation: I had the look of disgust on my face.

A few days ago, Sarah and the boys came home from a shopping trip. They went to the store to pick up a fun item that, in my opinion, would cost around $25. However, when they came home, they immediately said it had cost $110 instead. Whoa. That's a big delta between expectation and reality.

Sarah must have picked up on my lack of a good poker face. Translation: I had the look of disgust on my face. That wasn't my intention, but the cat was out of the bag. She immediately began throwing out next steps:

Take it back.

Subsidize this unnecessary purchase with her own personal spending money.

Make the kids save up and pay for a portion of it.

I quickly refused all of these options. Instead, I said we should keep this item and manage the monthly Kids spending category accordingly. This purchase, in and of itself, isn't a bad thing. Rather, what happens next will dictate that. That's the beauty of budgeting. Sarah can spend whatever she wants on whatever category she wants......as long as we don't overspend the categories. Therefore, even though she spent a TON on this item, it can still fit within the broader context of our budget. There's a cost. There's a consequence. Perhaps it means not buying the kids a pair of shoes. Perhaps itmeans we do a few less extra treats. Perhaps we go to one less kid's event. It's not about refraining from spending on "wants," but managing the puzzle pieces well.

Every category should be managed this way. Set a dollar amount, then live. Don't guilt yourself. Don't starve yourself of a purchase. Don't live in constant regret. Don't second-guess your partner. Set the budget, then manage the puzzle pieces accordingly. One of the best gifts I can give my wife is to entrust her to manage the pieces however she feels best. I don't question her purchases. I don't criticize her purchases. If she's managing the pieces well and we're staying on track, she's winning; we're winning.

Spouses, this might be what the doctor ordered to reduce financial tension in your marriage. We don't have to look over each other's shoulders. We don't have to question. We don't have to criticize. We don't have to live in fear every time an Amazon box shows up at the door.

Negotiate the budget each month. Set category-by-category targets.

Live your life.

Manage the pieces to fit life within the parameters you set.

Trust each other.

Track your spending along the way.

Know where you landed.

Repeat.

There's a freedom in not having to care about every expenditure our partner makes, trusting that by the end of the month, the targets set in the original budget have been honored.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

100% Ours

Tempers were flaring, f-bombs were tossed like hand grenades, and the occasional tears arose. This was the scene of a recent sit-down I had with a struggling couple.

Tempers were flaring, f-bombs were tossed like hand grenades, and the occasional tears arose. This was the scene of a recent sit-down I had with a struggling couple. The subject matter: the income differential between the two spouses. More specifically, how the couple makes financial decisions given their income differential.

Here's the high-level summary of the situation:

Husband makes 70% of the income, and the wife makes 30%.

The husband handles the day-to-day finances.

The husband's income pays for the family's needs, and the wife's income pays for the wants (travel, dining out, entertainment, etc.).

The husband spends anything he wants, but gives his wife "an allowance." After all, she only makes 30% of the family's income.....so this is generous (his words, not mine).

Every time there's an argument, the husband throws out the trump card: "I make more than twice as much as you, so I get to make the call."

As the conversation unfolded, the husband realized I must have had a look of disgust on my face at the words coming out of his mouth. He seemed surprised. After all, he knew that I was the breadwinner in my marriage. As such, I would naturally align with him, right?

By my records, I made 98.5% of our family's income in 2025. Translation: My marriage is far more unbalanced than his. With that context in mind, I explained to them (mostly him) that their way of handling finances is beyond toxic. They are keeping score with money and using it as a weapon. Further, their dumb idea of allocating her income to wants meant that if she ever wanted to take a different job or stay at home, she would be solely responsible for ripping all enjoyment and adventure from the family. Gross.

I may make 98.5% of my family's income, but our income is 100% "ours." Not mine. Not mostly mine. Ours. Everything Sarah and I make is viewed as a collective pot for us to manage together. Yes, I do the day-to-day finances. Yes, I createthe first draft of the monthly budget. Yes, I have more financial expertise than her. However, she ALWAYS has a 50/50 say in all we do. In fact, early in my marriage, I promised myself that I would never get more monthly personal spending money than she does. She would always get the same as me....or more on some occasions.

Something powerful happens when couples view money as a collective pot. It allows a full integration of life and decision-making. This income isn't for this, and that income isn't for that. It's just money in and money out. We're both called to different work in our lives, and in this season, my work provides 98.5% of our income. That doesn't make her less valuable or less impactful. It just means my work pays more. Sarah is impacting the world in different ways; important ways.

Whatever income dynamic you have in your marriage, I strongly (STRONGLY!!!) encourage you to adopt a "100% ours" mentality. You're a team, not a competition. Be in this together, side by side.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Got a Secret to Tell Ya

You know all the people in your life who look wealthy? They probably aren't.

Today is your lucky day, as I got a secret to tell ya. Ready for it? Okay, here goes. You know all the people in your life who look wealthy? They probably aren't. In fact, most people who look wealthy are far from it. I've worked with hundreds of families over the years, and this is a common and predictable theme.

They might have a lifestyle that suggests they are wealthy, but, in a fun twist of irony, these perceptions they create are among the factors that keep them from actually being wealthy. Cars, houses, clothes, trips, toys, technology, clubs....each of these externally facing expenditures puts pressure on finances (never mind the debt). Translation: In an attempt to look wealthy, people often sabotage the finances that might lead them to actually become wealthy.

I have a bonus secret for you! You know all the people around you who are just living normal underwhelming lives? A good chunk of those families are actually wealthy. They don't care what you, me, or anyone else thinks of them. They don't need to show off. They don't need to portray a certain image. They simply take care of their business and keep their heads down. These also happen to be the most generous people, too, as they don't feel the need to selfishly spend all the money on themselves.

Next time you see one of your friends, family, co-workers, or neighbors and think to yourself, "man, I wish I were as wealthy as they are," you might already be. You might think you want their financial life, but if you were to see what's on the other side of that curtain, it might make you grateful for the life you do have.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.