The Daily Meaning

Take your mornings to the next level with a daily dose of perspective and encouragement to start your day off right. Sign-up for a free, short-form blog delivered to your inbox each morning, 7 days per week. Some days we talk about money, but usually not. We believe you’ll take away something valuable to help you on your journey. Sign up to join the hundreds of people who read Travis’s blog each morning.

Archive

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- August 2021

- November 2020

- July 2020

- June 2020

- April 2020

- March 2020

- February 2020

- October 2019

- September 2019

A Middle Finger To Our Future Selves

To his detriment, he lived out the principles he preached way back then. He spent, spent, and spent, giving little regard for his future self.

I remember speaking to a colleague nearly 20 years ago. He was probably in his early 30s at the time, several years ahead of me in his career. While I wasn't necessarily the wisest steward with my financial resources back then, he and I shared many conversations that stopped me in my tracks. These conversations usually centered on the idea that we don't know whether we'll even be alive when we're older, so we might as well "enjoy life" while we're young. And by "enjoy life," he meant spend, spend, spend. He hated the idea of saving, or heaven forbid, investing. If he had it, he was going to blow it on something fun.

Fast forward 20 years, and I recently ran into him. He's now in his 50s, visibly older than when we last connected (as a few decades of life will do). This time, though, his attitude was different. He was asking me about retirement, investing ideas, and the worry about likely not having enough.

To his detriment, he lived out the principles he preached way back then. He spent, spent, and spent, giving little regard for his future self. In fact, I'd argue he gave his future self a hefty middle finger. It turns out, though, that one day, our present self becomes that future self. Today, he's the future self that younger him so blatantly disrespected.

He's scared....as he should be. His options are limited.....as expected. He feels trapped.....which is understandable. Now, his 50-something self is wondering how to navigate not only the present, but the future. He lived a lot of life in his younger days, but his current and future quality of life are very much in question.

This is a tough situation. I have so much empathy for people who face these realities. Unfortunately, I don't have a magic wand to wave for them. I can't undo their past mistakes. There's no magic pill or secret strategy to bridge decades of gaps.

No matter how old you are today, future you is depending on current you to make wise choices. Sacrificial choices. Loving choices. Be a good steward, not only with your finances, but with your body, relationships, children, marriage, and mental health. Future us is pleading for us to be better and do better. Their livelihood depends on it, and soon enough, that will be our present self. Be good to him/her.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

For What?

Enough is enough because enough is enough.

I received a question from a blog reader after yesterday's post. I don't know this man personally, but based on my handful of e-mail interactions, I respect him a lot. He's very insightful and always brings wisdom to the conversation. I also know by now that his intentions are always honest. Therefore, when he asked me a fairly intense question, I received it with the utmost respect and care.

In short, he asked why I'm so personally interested in my investments. It would appear to be an obvious answer, culturally and financially speaking, but he added some additional context based on my prior content:

I don't believe in retirement.

I don't plan to leave my children a large inheritance.

I believe and practice joyful and sacrificial generosity.

I'm anti-hoarding

I don't care to "build wealth."

Money, stuff, and status don't interest me.

Therefore, his sincere question has so much merit. If all that is true (and I testify that it is), why do I personally care about having investments? He didn't say this, but based on the fact pattern I shared above, it's possible that I'm a liar, a hypocrite, or don't quite follow the principles I teach. Again, this is me saying this (not my friend!). Why, then, do I personally care about investments?

I responded to his message, but after pondering it more, I thought it might make for an interesting blog post. Why do I believe all those things above, yet still have personal investments?

It's a two-part answer:

A day will come when I'm no longer physically or mentally able to do good work. I hope that time doesn't arrive until my 80s, but it will most certainly arrive at some point. When that happens, I want to ensure we can financially care for ourselves.

A day might come when I leave this planet before Sarah does. Statistically, men typically die sooner than women. As such, I want to make sure Sarah will be financially cared for after my passing.

Both of these factors lead me to pursue investment assets that can someday achieve one or both of these objectives. Something interesting happens along the way, though, when we perceive retirement investing through this atypical lens. The math looks different, easier. When you won't need retirement funds until later in life, the math says we need to contribute less money for a shorter period of time (since the wonders of compounding have more years to cook).

What that means in my household is that nearly eight years ago, we realized that if we are good stewards and ensure our investments are well managed, we might not need to contribute much more (if any) to meet our two long-term goals stated above. In other words, we're probably going to (eventually) be fine with what we already have invested, so investing more would only serve our own materialism, pride, or selfish endeavors.

Therefore, we made a very odd but definitive decision approximately eight years ago. We will commit to never investing again. No more contributions. No more pushing. No more building. No more more. Enough is enough because enough is enough.

It's a weird journey to follow, and oftentimes difficult given my strong bend toward finance and "winning," but living life with an external focus rewires our souls. It connects us to people unlike anything else I can compare. I'm not necessarily advocating that people try to adopt this way of viewing life, but perhaps it will give you something interesting to ponder today.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

OK, But Where You Gonna Get 9%?

The U.S. stock market has delivered a return of over 9% annually (and 10% annually over the last 100 years). Almost every time I discuss this topic, someone snidely asks, "OK, but where you gonna get 9%?"

My simplification of investing principles and practices is one of the most heavily criticized topics I write and podcast about. Here, I'll give you the quick elevator speech: Patiently invest in a cheap, broad, total U.S. stock market index fund. Invest early, contribute regularly, never sell, do nothing, remain patient, don't meddle, and let the market take care of the rest. See, simple! I've also written many times about how the 155-year history of the U.S. stock market has delivered a return of over 9% annually (and 10% annually over the last 100 years). Almost every time I discuss this topic, someone snidely asks, "OK, but where you gonna get 9%?"

That would be a fair question, except for the fact that we discuss it regularly! "A cheap, broad, total U.S. stock market index fund." Examples could include VTI, VTSAX, or FSKAX. This isn't a theory. It's not some hypothetical. It's not a case study that looks good on paper but is difficult to put into practice.

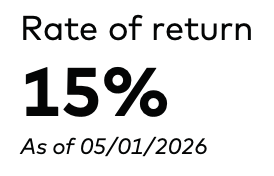

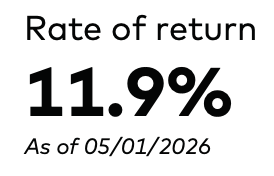

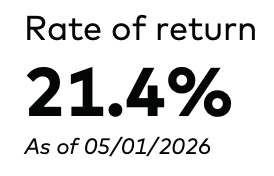

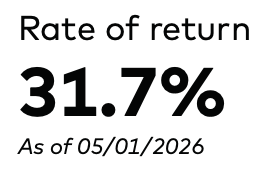

Today, I'll open the books of my life. For the past 15 years, my investment accounts have held one thing and one thing only: "A cheap, broad, total U.S. stock market index fund." I've made zero changes. I spend literally no time managing it. I give zero consideration to the ups and downs of the market. I never consider tweaking or meddling. What do I have to show for it? I'll show you.

My investment account updates the annualized return numbers at the end of each month. Given that April just concluded, I jumped into my account to see where they stand, and here's what I found:

Over the past 10 years: 15.0% per year

Over the past 5 years: 11.9% per year

Over the past 3 years: 21.4% per year

Over the past 1 year: 31.7% on the year

I'm not trying to beat the drum of "building wealth" or getting rich, but rather, I want people to understand 1) how real this is, and 2) how simple these principles really are. If we're going to invest, we might as well be good stewards of the resources we're blessed with.

Where you gonna get 9%? Right here. Right in front of us. While we don't know what the future will hold, the last 155 years tell us that, yes, it will be messy, but also yes, it will be rewarding. Stay patient. Stay simple.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Playing Us Like a Fiddle

I recently did a little informal survey on my Instagram account. Here was the question: "Without looking, how do you think the U.S. stock market has performed over the last 12 months?"

I love watching how the mainstream media and social media talk about the stock market. When the markets are going through a tough spell, people (hysterically) talk about it. The world is ending! The world is ending! You're all screwed!!! Yet, when the market is doing well, crickets.

I recently did a little informal survey on my Instagram account. Here was the question: "Without looking, how do you think the U.S. stock market has performed over the last 12 months?"

70% of respondents said the market was down. 20% said the market was up. 10% said it's about the same. On average, respondents said the market is down by approximately 9% over the past 12 months. How did they do?

At yesterday's market close, the U.S. stock market was up 32% over the past 12 months (up nearly 34% after accounting for dividends). Strange, isn't it? The overall sentiment is that the stock market is burning, while in reality, it's hitting new all-time highs. The stock market has nearly doubled over the past five years, yet we think the world has already collapsed.

They are playing us like a fiddle! From a behavioral science perspective, we see what we want to see. If we have a negative tint to our lens, we'll find the negative. If we have a positive tint to our lens, we'll find the positive. Today, our culture thrives on a negative lens, and the media all around us is more than happy to help us indulge.

One young man who answered my question guessed that the market is up 30%. He practically nailed it! I voiced my surprise that he knew this and shared why I was conducting this little study: "Oh, I don't watch the news or follow social media."

In other words, nobody played him like a fiddle. He was basing his answer on whatever information (you know, facts) he had available. He was able to cut out the noise, remove the biased lenses, and try to answer my question based on practical thought. Somehow, that's a crazy concept in modern-day America. It's a wild world when we can be more in tune with reality by absorbing less content.

One money-related takeaway. Open your investment account. See for yourself. If you're investing well (i.e., broad, low-cost stock market index funds), you should see your balances at an all-time high. Never before in your life have the balances been at this level. Celebrate that. Know it's true. Also know that rough times will, in fact, come. That's okay, though, as it's all part of the journey.

Lastly, and most importantly, try to muffle the noise, live a meaningful life, and don't let the day-to-day craziness of the media or the stock market mess with you. Life's too short to obsess over the things we can't control.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Reckless, I Guess

During that nearly 160-year stretch, from the late 1800s until today, the U.S. stock market has NEVER lost money over a 15-year period of time. Ever. Sure, history tells us that we could lose half of our life savings (on paper) over a five-year window.

One of my friends recently blasted me in a one-on-one conversation. Well, not me, specifically, but some of my content. He said that I "teach reckless principles" when it comes to investing. To summarize, I regularly talk about the simplicity, power, and effectiveness of investing in broad U.S. stock market index funds (such as VTI, VTSAX, FSKAX, VOO, or SPY).

My friend believes this advice is beyond risky. In his words, I'm "gambling" my life savings away.....and telling others to gamble, too. He's not alone in this sentiment, which is why I spend a large chunk of my professional and teaching life educating people about the truths of investing.

Did you know people owned stocks while they were still riding around on horses? Yeah, the U.S. stock market has been around since before the automobile was invented. We're talking Abraham Lincoln and the Civil War. That's what kind of track record we're talking about here.

During that nearly 160-year stretch, from the late 1800s until today, the U.S. stock market has NEVER lost money over a 15-year period of time. Ever. Sure, history tells us that we could lose half of our life savings (on paper) over a five-year window. That's happened in the past (1928-1932)... so there is precedent. But never in nearly 160 years has the market lost money over a 15-year period of time. The worst 15 years of all time were from 1929-1943, when the market delivered a total 19% gain over that stretch of time (1.15% per year). Considering what was happening in the world during that stretch (two World Wars!!!!), that's a pretty remarkable outcome!

One last number. The WORST 25-year period since the late 1800s saw the stock market increase by 3.3x (4.92% per year). Think about that. The WORST 25 years ever resulted in your investments more than tripling. Most people reading this article will be alive in 25 years. Historically speaking, your WORST outcome over that stretch will be tripling whatever you have today if you simply invest in a broad, cheap U.S. stock market index. It boggles the mind to even think about, and I don't think "reckless" feels like the right word to describe it.

This post isn't investment advice, but I did want to address this topic head-on while there's so much crazy noise spouting off all around us. We don't have to be scared. We don't have to play games with our investments. We don't have to take hot stock tips from Uncle Chuck at Thanksgiving or crazy Billy at work. Chances are, they will both be broke in due time. Instead, trust history, be patient, and don't lose sleep at night. It's always been a roller coaster and always will be a roller coaster, but if history tells us one thing, the roller coaster somehow finds its way uphill in the long run.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

If It Bleeds, It Leads

"Any thoughts on why the stock market is struggling so much right now? Do you think it will continue to be bad?" I stared at my screen for at least two minutes, trying to think of an adequate response. What in the world is he talking about?!?!

I received a text from a buddy yesterday. I haven't interacted with him much over the past six months, so he kinda caught me off guard:

"Any thoughts on why the stock market is struggling so much right now? Do you think it will continue to be bad?"

I stared at my screen for at least two minutes, trying to think of an adequate response. What in the world is he talking about?!?! My response:

"As of the closing bell last a few hours ago, the stock market is at the 12th highest price it's ever been in 155 years. What makes you think things are going so bad?"

"I've been seeing things about it on Twitter, TikTok and also the news. Everyone says it's bad and will keep being bad."

There's an old saying that's as relevant today as it was when originally coined: "If it bleeds, it leads." Fear sells. Fear triggers emotion. Emotion triggers reaction. Reaction triggers engagement. Engagement triggers revenue. Revenue triggers $. Translation: Fear = $.

We live in a fear-based society, and nowhere is this more true than in the reporting of financial markets. After all, it's really easy to report how bad things are when the market has a bad day. It's fun for the media to blast big red numbers on the screen, alongside a curated short-term graph that shows a jagged line moving in a down-and-to-the-right trajectory. Fear!

Truth is, the stock market returned 17.7% in 2025 and is up approximately 1% in this young year. The 12 best day-end stock market prices in history have all occurred in the last 31 days. Here, let me show a picture:

This is what the U.S. stock market has looked like over the past five years, yet at the same time, a huge portion of our society thinks we're in the middle of a crash. It’s literally lingering at the peak of the best price in human history, yet many people think we’re in the toilet. If it bleeds, it leads. Fear = $.

My biggest encouragement is to simply ignore the noise. We're not going to stop the media or people around us from using fear to manipulate our emotions. Therefore, we must insulate ourselves from the madness. I find it best to simply ignore it. Period. Live a meaningful life, make an impact on others, give generously, and enjoy some good food.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Here’s My Prediction

"What's the stock market gonna do this year?"

"What's the stock market gonna do this year?"

One of my friends asked me to look into my crystal ball and let him know what he can expect from his stock market investments in 2026. Here is my prediction: Somewhere between -40% and +40%.

He rolled his eyes at me, pointing out that that doesn't sound like an expert answer. Great observation, as any "expert" who claims to know what to expect is a fool, not an expert.

The market was supposed to get crushed in 2020 after COVID reared its head: it ended the year +18%.

The market was supposed to have a bad year in 2021 on the heels of an inflated 2020: It ended the year +28%.

The market performed as expected in 2022: it ended the year -18%.

The market was supposed to have a tough year in 2023: it ended the year +26%.

The market was supposed to have an even tougher year in 2024: it ended the year +25%.

The market was supposed to be devastated in 2025 (which seemed to be evidenced by the early 20% tariff-driven "collapse"): it ended the year +18%.

In theory, the market will get crushed in 2026. In practice? I guess somewhere between -40% and +40%. More importantly, nothing that happens during the year, good or bad, will influence my investing decisions or perspective. This year doesn't matter. Next year doesn't matter. All that matters is the big picture....decades.

Therefore, sit back, grab some popcorn, and enjoy the roller coaster ride. Oh yeah, and embrace your meaningful life along the way. Life is too short to worry and lose sleep over something we can't control.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Meddling

A close friend recently texted me and asked if I would share what adjustments I've been making to my investments. After all, the world is constantly changing! It's important that we tweak and optimize our investment portfolio, right?

With another year coming to a close, a close friend recently texted me and asked if I would share what adjustments I've been making to my investments. After all, the world is constantly changing! It's important that we tweak and optimize our investment portfolio, right?

I shared all my adjustments with him, and I thought I'd do the same with you. With that context in mind, I'm going to give you a detailed breakdown of all the adjustments I made in 2025:

My apologies, that was kinda boring. Perhaps you'll find 2024's adjustments more exciting:

Ok, this isn't helping. How about 2023:

The truth is, I don't tweak, optimize, mettle, or adjust. I simply invest broadly (and cheaply) in the U.S. stock market and allow time to run its course. Outside of rolling my former employer's 401(k) into my IRA nearly 7 years ago, I haven't made a single adjustment to my investment portfolio in 10+ years. It might even be 20 years, but my memory doesn't allow me to confidently testify to anything longer than a decade out.

If your investing isn't the easiest, simplest, and most hands-off thing in your life, you're doing it wrong. And by "wrong," I also mean poorly. Nothing good happens when we meddle. The best thing we can do is invest the right way and allowtime to pass. That's it. That's the secret.

If this is already what you're doing, congrats on your inevitable future (eventual) success. However, if everything I'm presenting seems foreign to you, perhaps now is a great time to reorient your portfolio and your perspective.

Have a very happy NYE!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Closer Than You Think

I have good news for you today. Strike that, great news!!!!! I have great, amazing, fantastic news for you today. If you've been trying to make progress on the retirement front but feel like you're not getting as far as you had hoped, you're probably closer than you think.

I recently stumbled upon a few surveys that were beyond concerning. Here are the headline numbers from each:

69% of American workers believe they could work until retirement age and still not have enough money to retire.

68% of Millennials don't believe they will ever be able to retire without receiving a meaningful inheritance.

Neither of these is surprising, but still concerning, nonetheless. Americans, on the whole, are tremendously underprepared for retirement. I feel that way on a family-by-family basis, and the average and median retirement savings numbers also back it up. We are woefully prepared for the next chapter of our lives, which is a deeply concerning trend.

However, I have good news for you today. Strike that, great news!!!!! I have great, amazing, fantastic news for you today. If you've been trying to make progress on the retirement front but feel like you're not getting as far as you had hoped, you're probably closer than you think.

Last week, I met with someone seeking investment advice. In his words, "I've been saving for nearly a decade, and all I have to show for it is $100,000. I'll never get to a million. I don't even feel like it's worth trying anymore."

My response: "Congrats, you're a third of the way there!!! Keep going!"

Him: ..............

Now, it's obvious that $100,000 is not 33% of $1M. Any idiot can tell you that. From a sheer dollar perspective, he's only 10% of the way there. However, investments (if done right) don't work on a linear scale. In the financial world, we call it compounding. When our money is invested, we make money on our money. Then we make money on our money plus the money we previously made. Then we make money on our money plus money on the money on the money. It's a cycle that speeds up over time.

Here, let me show you with an illustration. This is an example where someone invests $500/month and earns an average of 9% per year over the long run. We obviously won’t earn a consistent 9% over time (it will be a bumpy road for sure), but this makes for a useful visual:

As you can see, it takes a little more than 10 years to accumulate the first $100,000. That was the hardest part, and often where people get frustrated and give up (i.e., the studies referenced above). However, because of the power of compounding, the second $100,000 only takes five-ish years (half as long!). The third $100,000, only 3.5 years. All the way up until that last $100,000, which takes just over a year to complete. From a time perspective, you're halfway to your $1M goal by the time you hit $200,000. Crazy!

This is a concept that's hard to wrap our minds around, but is so freeing once we do. I do my best to beat this into the head of anyone who is feeling discouraged by the process. It's so easy to give up along the way if we don't understand just how powerful this compounding thing will eventually become.

Don't be discouraged. Have a sense of urgency, yes, but don't feel defeated. Keep pushing through, and let compounding do the heavy lifting for you.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Gambling vs. Investing

Based on available data, 94%-95% of sports bettors lose money. Remember when Uncle Johnny crushed that four-team parlay and did shirtless victory laps around the house?

I recently went on a tirade against sports gambling amongst a group of friends. I firmly believe that we will look back 20 years from now and realize that sports gambling took down an entire generation. It's literally crippling people. Not rare, random people who are far removed from us. I'm talking about our friends, family, co-workers, and neighbors. Behind closed doors, sports gambling is pilaging families of their resources all around us......perhaps even in your home.

Something happened immediately after this recent tirade, though. My friend essentially called me a hypocrite. Why? Not because I gamble.....I won't even put a penny into a slot machine. I'm a hypocrite because, in his words, I "talk so much about investing on my podcast and blog."

Everyone at the table agreed with him, too. Whoa. That's wild to me. I had to catch my breath after that one.

They explained that investing is 100% gambling. The same principles are at play, but I'm just gambling on companies instead of sports teams. In their minds, whenever we invest money into the stock market, we're gambling, and there's a very real chance we'll lose money.....just like when they throw money at the sports books.

What do the numbers say? First, sports betting. Based on available data, 94%-95% of sports bettors lose money. Remember when Uncle Johnny crushed that four-team parlay and did shirtless victory laps around the house? Yeah, that was a short-term win amongst a longer-term loss....he just conveniently failed to volunteer that little tidbit with you. The data shows that almost every single person will lose money over time. It's the rare 1 out of 20 people who can perpetually pull profits from their betting app.

Now, the stock market. In the 155 years of stock market existence (almost back to the Civil War), there has NEVER been a 15-year window when the stock market lost money. Never. In other words, over a span of 15+ years, 100% of investors who invested the right way would have turned a profit. To further add salt to the investing vs. gambling wound, the worst 30-year window in stock market history provided a 4.4x return. Yes, you would have quadrupled your money over the worst 30 years in U.S. history. That doesn't sound like gambling to me!

Is investing like gambling? They couldn't be more different. Gamblers are nearly guaranteed to lose money, while investors are historically guaranteed to make money. If that doesn't paint the picture, I don't know what will.

Seriously, though, if there's gambling happening in your house, I implore you to reconsider. I'm watching families and marriages melt before my eyes over this stuff. I'm witnessing households get further and further behind on their finances, at the mercy of gambling activity. I'm seeing cash get pushed into gambling apps instead of into 401(k) plans and IRAs. It will eventually catch up with people, and by the time that happens, it will be far too late to remedy it.

Investing (the right way!) has proven again and again to be a safe, reliable, and powerful part of every family's long-term journey. Please don't let that opportunity pass you by.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Embracing the Chaos

But what about 8-10%!?!? Isn't that what we should use to gauge performance? Yes....and no. Let's play a little game. In the last 155 individual years, how many years did the stock market finish in the positive 8%-10% range?

"My investments are doing awesome!" exclaimed one of my friends. I was having drinks with an old friend when he brought up the topic of investing. I'm always interested in context when these types of comments are made, so I inquired. "Why do you say that?"

He shared that he had just recently met with his financial advisor. Over the last two calendar years, his investments were up about 12% each year, and he's on track to do that again this year.

I don't have a great poker face, so he could immediately see the look of disgust on my face. "If the market is supposed to get 8%-10% per year, my last two years have been pretty awesome! There's no disputing that."

Here's the truth. In the two years he just reported to me, 2023 and 2024, the U.S. stock market was up 26% and 25%, respectively. With that context in mind, yes, his 12% performances were absolute trash.

But what about 8-10%!?!? Isn't that what we should use to gauge performance? Yes....and no. Let's play a little game. In the last 155 individual years, how many years did the stock market finish in the positive 8%-10% range?

Three times. Three times out of 155 years. 1912, 1916, and 1993. That's it. Those are the only three years in U.S. history that actually finished in the 8%-10% range. With that being said, the market is up an average of 9.2% per year over the past 155 years (and 10.3% per year over the last 100 years).

This is one of the most important concepts we need to understand. It's not about trying to get 8%-10% on any given year. Rather, it's about meeting the market embracing the chaos......which is what eventually brings us to 8%-10%. As an example of this concept, here are a few fun facts about the last 155 years:

As already mentioned, the stock market has achieved 8%-10% only three times.

The market has finished +20% or better 49 times, which is roughly once every 3 years for one-and-a-half centuries.

The market has finished -20% or worse 8 times.

It's a wild ride! If 2025 ended today, the market would have achieved an average annual return of 14.5% over the last decade. However, look how messy it's been:

2016: +11.8%

2017: +21.5%

2018: -4.3%

2019: +31.1%

2020: +18.1%

2021: +28.5%

2022: -18.1%

2023: +26.0%

2024: +24.8%

2025: +16.9%

See, wild ride! The only way for us to get our desired long-term results is to experience the full weight of the chaos on the upside, endure the inevitable chaos on the downside, and know that it will average out to something beautiful.

However you handle your investments, whether on your own, through your work's retirement plans, or via a financial advisor, don't measure your short-term returns against some arbitrary target. Instead, we should endeavor to meet the market and embrace the chaos, for better or worse. It will rarely look like 8%-10% in the short-term, but if we're willing to embrace the chaos, we'll eventually be rewarded handsomely for our discipline and patience.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Turns Out Old Isn’t Old

My friend had a different philosophy of life. In his words, we might die tomorrow, so we might as well have as much fun as we can now. And even if we don't die tomorrow, why wait until we're 50 or 60 to have fun, since we'll be too old to enjoy ourselves by then anyway.

Let's rewind the clock 20 years. It's 2005. Times are good. The economy is booming, and we haven't yet experienced the wrath and destruction of the Great Financial Crisis. I was 24 years old, new in my young career.

One of my friends was about six years older than me.....right around 30. Over drinks, we shared a conversation that I've periodically thought about for two decades. It's a conversation that might hit close to home for you. My friend was known to be impulsive, the proverbial life of the party. During one of our conversations, the topic of money came up. While I wasn't making the wisest of financial choices back then, I did understand one important concept: Investing for the future is imperative.

My friend had a different philosophy of life. In his words, we might die tomorrow, so we might as well have as much fun as we can now. And even if we don't die tomorrow, why wait until we're 50 or 60 to have fun, since we'll be too old to enjoy ourselves by then anyway.

Nearly twenty years have passed since that conversation. Guess where my friend is today. He's 50.....and healthier than ever. In his words, he's at the peak of his life. Just one problem: His 30-year-old self took that perspective seriously and thoroughly enjoyed life, leaving nothing for "old" him. Today, he sits at 50 and has no idea what his future will hold. Life is full of doubt, uncertainty, and stress. Will he have to work involuntarily forever? How will the bills be paid? There's not enough money to save for the future and actually enjoy life today.

I feel so terrible for him and his situation. He's between a rock and a hard place, and unfortunately, there's no redo button. That's the problem of having the attitude he had when he was younger. We ALWAYS become future us. Current me will someday become future me. A time will come when I am forced to live in the reality established by younger me. On one hand, that's the scariest concept in the world. On the other hand, it's so empowering.

Every day we wake up, we have the power to help future us. Each positive step we take is a blessing for future us, while each mistake is a curse for future us.

Yes, you're younger today than you will be someday. At the same time, however, 20 years from now you'll still be younger than you will be someday. Current you is always the youngest version of you. Please help yourself help yourself. Your future self will thank you.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Hyperbole For the Masses

Plunged. Tumbled. Sank. Crashed. Tanked. The media has had no lack of hyperbolic words to describe what happened to the stock market on Friday.

Plunged. Tumbled. Sank. Crashed. Tanked. The media has had no lack of hyperbolic words to describe what happened to the stock market on Friday. People are losing their minds! If you aren't aware, the U.S. stock market fell by approximately 2.7% on Friday. Based on the dozens of texts I've received since then, many people are anxious.

"Market Falls Off a Cliff," reads one international news outlet headline. If you're casually scrolling the web, what do you do with a headline like that? I'll tell you what many people do. They start to get scared. Is it warranted? Should people be worried? Is now a great time to be fearful?

Well, it depends on what your goals are. If your goal is to never see your account balance fall below where it is today, then yes, you should be terrified. However, if your goal is to end up in a good spot years or decades from now, no, you shouldn't be worried in the least.

One of my friends specifically asked about how badly the stock market got crushed on Friday. After all, the hyperbole used to describe those events makes it sound like doomsday. Please allow me to put it into perspective. After the market fell by 2.7% on Friday, we are down to a level that had never before been achieved since the Civil War.....until 9/11/2025. That's right. The price of the stock market today is at level that was an all-time high less than a month ago. Here, maybe this chart will serve as a clear visual:

This chart illustrates what the last five years have looked like for the U.S. stock market. That tiny little blip in the upper right-hand corner of the chart is Friday's "plunge." It's about as scary as a Halloween-themed show made for toddlers.

Will the stock market experience a far more significant decline? Probably. When will it happen? No clue. None of that is important, though. What's important is that we continue to practice the "do nothing" strategy and simply live our meaningful lives. Let the market be the market because the market is always the market. P.S., that's a good thing. We have the greatest stock market that has ever existed, and 155 years of proven data to back it up. Therefore, I love letting the market be the market because the market is always the market.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

The Benefit of Hindsight

"You can't invest today in good faith. The &%$#@!& market is far too expensive. Every dollar you put in is begging to be lost. Stop giving your readers &@$#% advice!"

I received several angry messages from buddies regarding my recent post about why we shouldn't time the stock market. These buddies, of course, are "investing experts." They are mirror images of the man I covered in the previous post. They believe what he believes and acts as he acts. Here's what one of them said (excluding the expletives):

"You can't invest today in good faith. The &%$#@!& market is far too expensive. Every dollar you put in is begging to be lost. Stop giving your readers &@$#% advice!"

I present to you Exhibit A:

This is a graph of the U.S. stock market (S&P 500) since 1/1/2000. As 2000 unfolded (far left side of the graph), due to the tech bubble, the stock market hit unprecedented levels of "too expensive." The market was clearly overvalued, and experts warned that it was too high to justifiably invest.

Do you see where this is going? Yeah, while the market felt a bit rich in 2000, with the benefit of hindsight, it now looks cheap. In fact, today, the stock market is 4.4x higher than it was at the peak of "too expensive" in August 2000.

It's not all roses and sunshine, though. What you'll see if you look close enough at this graph are the following rough patches:

46% loss after all-time high in August 2000

54% loss after all-time high in October 2007 (second-worst crash in history)

32% loss after all-time high in January 2020

25% loss after all-time high in December 2021

20% loss after all-time high in January 2025

And today, after the stock market hit a new all-time high in September 2025, we're back in the same position. Will we get our butts kicked again? Absolutely! However, with the benefit of hindsight, today's all-time high will eventually look cheap.

I say it over and over again, but please don't let the naysayers (or "experts") scare you into fear-based decisions. History always has a way of taking care of itself.....eventually. The benefit of hindsight will soon prove your patience right.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Someone Should Check On Him

My buddy had personally lost $200,000 (around 17%) and was now sitting on about $1,000,000 of cash in his portfolio. According to him, he was going to let the market continue to crash, and he would swoop back in to "buy the dip."

I had a doomed conversation in early April. One of my friends, a self-described investing expert (but with a bunch of suffixes after his name to back up his mouth), made a dire proclamation to me. In his words, "the stock market meltdown has begun.....it's time to go all cash." Translation: He, in all his brilliance, was predicting an immediate, all-out stock market crash and planned to sell all his investments to avoid losing money. Further, with his masterful wisdom, he was telling everyone around him (including me) to do the same.

Here's some added context. When he shared his "expertise" with me, it was in the midst of the great tariff scare of 2025. The stock market had experienced a few bad weeks, and people were anxious. The overall stock market was down nearly 20% from the all-time high it experienced just six weeks prior. That's when he sold.

My buddy had personally lost $200,000 (around 17%) and was now sitting on about $1,000,000 of cash in his portfolio. According to him, he was going to let the market continue to crash, and he would swoop back in to "buy the dip."

Five months have passed since he made this decision. Wanna know where we stand today? The market is up approximately 40% since he sold all his investments. 40%!!! The market has hit 24 new all-time highs since his bold proclamation, including a new one yesterday afternoon.

Had he simply done what actual wise investors do (nothing!), his $1M portfolio would be up by $400,000. In his desire to be smarter than everyone else and try to play games with the market, he lost out on $400,000 (!!!!) of upside. All he had to do was nothing. Literally, nothing. When I explained to him that his strategy has a terrible historical track record, he laughed. Today, he's $400,000 poorer because of it.

Someone should check on him. Well, I actually did yesterday. Let's just say "frustrated" would be a gross understatement to describe his state of being. He was so sure he was going to outsmart the market this time. He would have bet his life savings on it. Strike that, he did bet his life savings on it.....and lost.

He's at a loss on how to move forward. Does he now wait until the market falls? Does he just lick his wounds and get the money back working for him? Both options feel like a loss to him. These are the psychological implications of trying to play these sorts of games.

Here's what I told him: "What's done is done. You can't go back and get a redo. However, you can promise yourself you'll never do this again. Call it an expensive lesson. Humble yourself. Don't try to be smarter than everyone else. Invest your money and leave it invested. The market will take care of the rest....eventually."

We'll see where he goes from here, but it's a cautionary tale for all of us. The best investors in the world are the ones who know they aren't smarter than the market. Patience beats brains every day of the week. I have 155 years of history to prove it. Today is a great day to do nothing, and tomorrow is a great day to do nothing, too.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Well, Well, Well Again

In the entire investment world, there are only a few dozen people who can be successful at this for an extended period of time, and they aren't your brother's co-worker's neighbor. It's not your financial advisor, either!

In my June 28th post, I discussed how the U.S. stock market had just hit a new 155-year all-time high. More importantly, I reiterated that an all-time high isn't something to be scared of. In the post, I detailed how frequently our stock market hits new all-time highs, and why that's just a regular feature of long-term investing.

Without fail, I received nearly a dozen messages pushing back against my message. One person told me I'm "stupid." Another told me I'm "naive." A third told me I'm "uneducated." That was a fun day to open my inbox!

Lots of people (who claim to be wise investors) get on their soapboxes and tout the strategy of "buy the dip." In other words, try to time the market by investing after it crashes. That would be an amazing strategy if we had a magic 8-ball or DeLorean. The problem with timing the market is that we must be right twice: first, when to buy, and second, when to sell. Besides, that's a stressful and time-consuming endeavor. In the entire investment world, there are only a few dozen people who can be successful at this for an extended period of time, and they aren't your brother's co-worker's neighbor. It's not your financial advisor, either!

Since I wrote that post on June 28th, the U.S. stock market has achieved another 12 all-time highs: One in June, 10 in July, and one in August (yesterday!).

Once in a while, my friend Brett will respond to a post with a simple question: "Where's the meaning in this post?" While today's post isn't jam-packed with meaning, I do have one very strong, meaning-filled encouragement. Please don't spend your time, energy, stress, or anxiety worrying about your investments. Simply invest in the U.S. stock market via low-cost index funds, be patient, and stop thinking about it. You have so many more important things to think about in your life than the fate of your investments. Their fate is awesome......long-term. Instead, invest your time and energy in your family, your work, your relationships, and your ministry. The ROI of those things is far greater than money will ever provide!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Blood Money

One reader took exception to my analysis and aggressively came to the defense of my friend. "You're a finance guy, Travis. You know the math. If your friend invests $850 each month for the next 25 years, that's $1,000,000. That's how he gets to create generational wealth. He'd be stupid to throw away that opportunity."

I've received countless thoughtful responses to yesterday's post about my friend who turned down his dream job because it would require him to effectively take a $850/month pay cut. His dream, calling, and aspirations were sitting right in front of him, and all he had to do was say "yes." He said "no." Money overcame meaning. He knows that, and he also recognizes that the societal pressures all around him were the driving force for his ultimate decision.

One reader took exception to my analysis and aggressively came to the defense of my friend. "You're a finance guy, Travis. You know the math. If your friend invests $850 each month for the next 25 years, that's $1,000,000. That's how he gets to create generational wealth. He'd be stupid to throw away that opportunity."

The math is correct. $850 contributed per month, at a 9% annual return, for 25 years (300 months), would result in about $950,000. He's absolutely right.

You know what I call that? Blood money. If my friend throws away his dreams, calling, and aspirations for the next 25 years (from age 42 to 67) and instead hoards all of this excess money, he'll end up $1M richer. Last time I checked, he only gets one life. One chance. One opportunity. One shot at this. And he's going to exchange the 25 most productive years of his life for a million dollars?!?!? Blood money!

If you know me (whether personally or through the blog/podcast), you know that I'm a big believer in investing. I teach it, advocate for it, encourage it, and help people execute it. I'm a staunch believer in the power of long-term investing. However, NEVER at the expense of meaning and impact. If our investing prevents us from living a meaningful life or it's at the expense of making an impact on others, it defeats the purpose.

Money for money's sake is like losing the game in the first quarter, but not yet knowing you lost. It's the kind of loss that sneaks up on us and blindsides us just as we thought we were about to win.

Sure, my friend could elect to invest $850/month for the next 25 years by turning down his dream. It will result in a million dollars. That's real money. Alternatively, he could live with meaning and follow his dream, calling, and aspirations, and undoubtedly live an amazing life. Not 25 years from now when he has a ton of money, but today. Today. Tomorrow. Next week. Next month. Next year. Always.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

What’s Under the Hood?

"If the stock market is at an all-time high, shouldn't my retirement account also be at an all-time high?"

After my recent post titled "Well, Well, Well," I received a sharp but appropriate question from a handful of readers. Here's how one reader phrased it: "If the stock market is at an all-time high, shouldn't my retirement account also be at an all-time high?"

Yes, yes it should. As of this moment, the U.S. stock market is still hovering around its new all-time high. Even if you haven't contributed any money in the last few years, your investment portfolio should be at an all-time high. However, if you've been consistently investing through the recent market turmoil, you should be crushing your previous all-time high,without question.

If you're one of the many people who are still not at all-time highs, there are a few reasons this could be (none of them good):

You're paying ridiculous, unnecessary, and possibly invisible fees.

You're implementing a sub-par strategy. I say "sub-par" through the lens that no strategy exists that will reliably match the returns of the overall stock market over the long run.

You're investing in the wrong funds. There's a LOT of trash out there, and most people (probably 90%) are invested in trash. Nearly every investing platform has a great S&P 500 index or total U.S. stock market index. These are broad, beautiful, and simple options.

You (or someone managing your money) is trying to time or game the market. This is a losing strategy.....period.

If you're interested in one additional piece of information to compare your portfolio to, here you go. Here is the annual return of the entire U.S. stock market over varying periods of time, as of 6/30/2025:

To put this into context, the annual return over 15 years was 14.43%. That means, over a 15-year period of time, the market increased an average of 14.43% every year. A $1,000 investment would have turned into $7,500. That’s huge! And it was right there for each one of us.

Those are some pretty ridiculous numbers. I encourage you to open your most recent statement and compare your portfolio's performance with these. If they are close, excellent! If they deviate from what you see here, please know a few things:

You are leaving tens of thousands, hundreds of thousands, or millions of dollars on the table.

You deserve better.

Having better is as easy as a few clicks on a screen. In today's financial system, nearly all investment platforms (including your company's 401(k)/403(b) offer at least one solid broad index option.

In my opinion, this is the simplest and biggest needle-mover most families have at their disposal. Money isn't always an easy topic, but in the case of investing, this is actually the easiest component to get right. Please don't let paralysis prevent you from maximizing your opportunity with the resources you've worked so hard save.

Perhaps it's time to log into that investment account and see what's under the hood.

For those who have asked, I only have one thing under the hood of my portfolio. VTSAX, which is Vanguard’s total U.S. stock market index (3,600 different companies). 100% of my family’s retirement resources are in this, and have have been for many years. Before that, my 401(k) lived in an S&P 500 index fund. As simple as it gets!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Well, Well, Well

And just like that, the U.S. stock market is at a new all-time high. Remember just two months ago when people were decrying the end of America and the utter destruction of millions of Americans' retirement accounts? Those were fun times.

And just like that, the U.S. stock market is at a new all-time high. Remember just two months ago when people were decrying the end of America and the utter destruction of millions of Americans' retirement accounts? Those were fun times.

Yesterday afternoon, the S&P 500 closed at $6,173, which marks a new 155-year high. The previous all-time high was $6,144, achieved on February 19, 2025.

Now, in a stunning and ironic twist, the same people who were decrying the end of capitalism (and subsequently and irrationally liquidated their investments out of fear) are now claiming it's a terrible time to invest since the market is so high.

You want to know the best time to invest? I'll tell you the secret. Lean in closer. Today. Today is the best time to invest.

"Yeah, Travis, but it doesn't make sense to invest at all-time highs. It's better to wait until it comes back down!"

If someone has a magic crystal ball that will perfectly predict the future, I'd love for them to share their secrets with me. Unfortunately, history hasn't boded well for people who tried to time the market. It's easy to look back with hindsight and declare what's what with uber confidence. Again, unfortunately, I don't see many people with DeLoreans parked in their driveways that allow them to go back in time.

Here's the truth. Yes, the market just reached a new 155-year high. However, it shouldn't scare us as much as people lead us to believe, for one very important reason. We hit new all-time highs all the time! For example, over the last 155 years (since the conclusion of the Civil War), the stock market ended the year at an all-time high 57 different times. That's one out of every 2.7 years. Here's how many times the market ended a year at all-time highs, by decade:

1870s: 2

1880s: 2

1890s: 1

1900s: 7

1910s: 0

1920: 4 (Roaring 20s)

1930s: 0 (Great Depression)

1940s: 0 (World War 2)

1950s: 7 (post-war boom)

1960s: 6

1970s: 1

1980s: 9

1990s: 8

2000s: 0 (tech bubble burse, 9/11, Great Financial Crisis)

2010s: 5

2020s: 5 (so far, including this year)

Imagine having a drink with a couple of buddies on New Year's Eve, 1968. You start discussing the stock market. One of your buddies begins talking about how the market feels too rich for his blood. After all, it hit new all-time highs in 13 of the last 18 years. It's now worth nearly $104!!! It's too high. It just doesn't make sense! We should probably wait for it to come back down.

You know better, though. Yeah, it's true the market hit new all-time highs 13 out of the last 18 years, but you also know the best time to invest is today. So, despite your friend's negative outlook, you invest anyway. Fast forward to today, whatever you invested on NYE 1968 is now worth 59x what you paid for it (plus all the dividends you received in the meantime).

Back to June 2025. Yes, we're at a new all-time high. Yes, the market will likely go down at some point. Yes, terrible things will happen in the meantime. And yes, we'll hit many, many more all-time highs. History has given us a road map to the future. All it requires of us is to be patient and enjoy the bumpy ride.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

They Shot the Elephant

In a recent meeting with one of these couples, I was writing a bullet list of possible uses for their taxable investment account. As soon as I wrote the word "pre-60 retirement," they asked me to erase it. "We don't want to retire. We like to actually live our lives and have purpose."

When I'm sitting face-to-face with most coaching clients, there's an elephant in the room. This person (or persons) desires to retire one day. They'll tell me, "We want to retire in 15 years." They might be 40 years old, meaning their objective is to prepare themselves to retire by age 55.

This desire has many implications. First, it means this couple needs to invest like crazy. They need to intentionally and repeatedly set aside large chunks of money each month as they race the clock to accumulate enough resources to meet their objective.

When they elect to set aside massive resources for retirement (you know, to win the race), this, too, has implications. It means fewer financial resources available to the family month in and month out. That may mean less fun, fewer vacations, less generosity, and a more frugal lifestyle. It might also mean they linger in higher-paying, lower-meaning jobs. After all, what's the point in pursuing work that matters if we're busy racing toward the finish line and stop working as quickly as possible? There's a conscious trade-off between finding meaning in their life now (which they might not) and hurrying toward the retirement finish line.

The financial and career pressures begin to build, all for the sake of meeting these age-based retirement goals. Some people enjoy this process, but most don't. In fact, it can turn a frustrating endeavor into a pressure cooker of stress, weight, and disappointment.

Then, there are meetings where I sit face-to-face with a different kind of client. This is the type of couple who, like me, have zero desire to retire. Both spouses are pursuing work that matters, enjoying the journey, and living with meaning every step of the way.

In a recent meeting with one of these couples, I was writing a bullet list of possible uses for their taxable investment account. As soon as I wrote the word "pre-60 retirement," they asked me to erase it. "We don't want to retire. We like to actually live our lives and have purpose." I love it!

The implications of this mindset shift run deep. Immediately, we were able to pivot our approach and create a weird and counter-cultural way to approach this topic. Every ounce of pressure and urgency melts away, as there's no defined race to run. Instead, we can plan more intentionally and weave all the pieces together in a way that creates a cohesive lifestyle (not just someday down the road, but today). There is no elephant in the room; they shot the elephant!

Instead of allocating massive sums of resources to retirement, they can take a more measured and flexible approach. They can allocate more money for memories, travel, and giving. Their investments, instead of needing to fund an ever-earlier retirement, can now feed more meaningful endeavors. Their career decisions can be centered around meaning, not paychecks. More than anything, there's no weight. They are going to be great. They don't feel burdened or heavy. It changes everything!

I shot the elephant years ago, and I'm so glad my client did, too! When we can untether ourselves from the race toward retirement, it literally changes every single aspect of our lives. So beautiful! Is it something you'd consider? Please think about it, and we'll talk about it again soon.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.