The Daily Meaning

Take your mornings to the next level with a daily dose of perspective and encouragement to start your day off right. Sign-up for a free, short-form blog delivered to your inbox each morning, 7 days per week. Some days we talk about money, but usually not. We believe you’ll take away something valuable to help you on your journey. Sign up to join the hundreds of people who read Travis’s blog each morning.

Archive

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- August 2021

- November 2020

- July 2020

- June 2020

- April 2020

- March 2020

- February 2020

- October 2019

- September 2019

Chicken or Egg?

I recently stumbled upon a heated online conversation on a social media platform. The original poster posed a question: "If so many people are struggling right now, why are there so many people with brand-new vehicles parked in their driveways?"

I recently stumbled upon a heated online conversation on a social media platform. The original poster posed a question: "If so many people are struggling right now, why are there so many people with brand-new vehicles parked in their driveways?" It seemed counterintuitive, as these new vehicles are presumably evidence that people are doing well.

Let's just say the comments were lively. Hundreds of people chimed in, positively confirming that most people are, in fact, doing great. The commenters believed they, individually, were simply part of the small share of people who are struggling, while everyone else is thriving.

I have news to break to them (and anyone else who will listen). Those brand-new vehicles sitting in people's driveways aren't evidence that people are doing great. Rather, those same vehicles are one of the primary culprits for why people are struggling so much. People's vehicles are putting them into a financial grave, month after month.

I recently met with a successful-looking couple who, from the outside, appear to have it all put together. They are fit, their kids are cute, their house is immaculate, they have good jobs, and they both drive new vehicles. The subject of the conversation? How they can stay financially afloat and not lose everything. Truth be told, their monthly finances didn't contain many red flags. Lots of normal, but not outlandish spending allocations. However, there were two major red flags.....and both were parked in their garage:

His vehicle: $1,100/month payment

Her vehicle: $850/month payment

Total vehicle payments of $1,950. In my brain, that's called a mortgage payment. Two thousand bucks for vehicles!?!? Both assured me that 1) they can afford them, 2) they are perfectly reasonable vehicles, and 3) everyone else has at least as nice vehicles as they do.

They aren't alone. This is a dynamic I see every single week in my coaching work. I've met with hundreds of families, and vehicle tension is the leading contributor to financial pain, suffering, tension, stress, and destruction. Not a lack of income, student loan debt, a failure to budget, or limited financial literacy. Vehicles. Vehicles are literally milking an entire society dry.

Many people who read this piece will roll their eyes at me. This topic often draws the ire of those who digest my content daily. That's okay, though, as this message needs to be shared over and over and over. I so badly want people to live a quality of life, and if I can get them to make different decisions in this vehicle department, I strongly believe it will have a direct positive impact on their quality of life.

We need more humility. We need more patience. We need to care a whole lot less about what others think. That's the ticket to some beautiful things in our lives. Please don't allow a vehicle to play a significant role in your journey. It can play a role, but not a leading role. You deserve better; much, much better!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Enjoy the Suck

If all goes well, by year-end, one of my clients will have paid off $48,000 of consumer debt in just 19 months. Two vehicles and a collection of student loans; normal stuff! They don't realize it yet, but their lives are about ready to shift into an exciting and unprecedented new realm. Nothing will ever be the same.

If all goes well, by year-end, one of my clients will have paid off approximately $50,000 of consumer debt in about 18 months. Two vehicles and a collection of student loans; normal stuff! They don't realize it yet, but their lives are about ready to shift into an exciting and unprecedented new realm. Nothing will ever be the same.

Whenever I bring up the idea of paying off debt to couples, most people say some variation of, "I don't want to throw away x years of my life." Translation: the only way to pay off debt is to not spend money on fun, and not spending money on fun is akin to wasting life and living in misery. Therefore, the juice isn't worth the squeeze. They would rather just enjoy life while they can, and kick the can down the road.

I've watched dozens (or hundreds) of families turn their backs on a significantly better life simply because they don't want to endure a season of sacrifice. The long-term implications of those decisions are catastrophic.

I have a little secret for you. Making sacrifices for a season to achieve a goal doesn't have to be a soul-sucking, fun-hating, misery-inducing journey. Sarah and I spent 4.5 years paying off $236,000 of crappy debt. It was the first 4.5 years of our marriage. And to be honest, the life we lived was pretty dang awesome. Did we make sacrifices? Oh yeah, brutal sacrifices. However, those sacrifices didn't define our quality of life or the meaning we experienced. Our standard of living sure suffered, but the quality of life was outstanding. We enjoyed the suck!

Today, when I look at young couples like my client mentioned above, I can't help but smile, knowing something they don't yet know. What lies on the other side of cleaning up this debt mess is a life they never knew existed. I can testify that this young couple hasn't stopped living life. In fact, I think they enjoy the suck, too! They have threaded the needle of making massive sacrifices while also enjoying their young marriage. In a few years, they will thank their former selves for paying the price for their freedom.

Enjoy the suck! Whatever sacrifice current you needs to make for future you to have a better life, do it! Don't wait. Life can be hard now or life can be hard later.......choose your hard. Sarah and I chose to enjoy the suck early. My young friends chose to enjoy the suck early. What will you choose? There's no better time to go for it than today.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Even More Reason

"What, so if you don't have $50,000 in the bank, you shouldn't buy a car?" my friend asked. "No, if you don't have $50,000 in the bank, you most certainly shouldn't be spending $50,000 on a car," I replied. His eyes got big, and he looked visibly agitated.

I ran into a buddy at the gym yesterday, and the first thing he said to me was about yesterday's post: "What if you don't have $50,000?" It was a reference to my story about the pile of cash test, where I challenged a client to withdraw $50,000 from the bank and set it on their kitchen table before officially deciding to put $50,000 toward a vehicle.

"What if you don't have $50,000?" It's a logical and realistic question, as $50,000 is a lot of money and many people simply don't possess $50,000. My answer?

"Even more reason not to do it!!!!"

"What, so if you don't have $50,000 in the bank, you shouldn't buy a car?" my friend asked.

"No, if you don't have $50,000 in the bank, you most certainly shouldn't be spending $50,000 on a car," I replied. His eyes got big, and he looked visibly agitated.

This isn't really about cars, though it's framed through the lens of a car purchase. At the heart of the matter is our modern-day assumption that we all deserve to buy whatever we want, regardless of context or reality. And debt allows that to happen.

I reminded my friend that the most money I've ever spent on a vehicle was $20,000. Why? Because that's how much money I had allocated and saved for said purchase. I suppose I could have pulled the trigger on a $50,000, $60,000, or even $80,000 vehicle had I wanted, but sabotaging my family's finances, freedom, and future with large debt payments isn't on my wish list of life. Instead, we buy what we can afford. That applies to cars, sure, but it's also a blanket statement of life. No debt.....period.

I know this is a weird way to approach life, and for many, it might seem limiting. However, there's something beautiful that happens to our psyche when we live in reality. It's powerful to know what's on the table and what's not. I don't think about buying luxury cars because it's simply not in my family's budget. Thus, I don't want. I don't covet. I don't fantasize. Instead, I try to live a meaningful life and embrace whatever beautiful reality we've created for ourselves. I encourage you to do the same.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

$50K On the Kitchen Table

"I don't care if you buy this vehicle," I told them. "However, if you decide to buy it, use cash. Please don't fall into this trap again."

More than three years ago, I wrote about something I call the "pile of cash test." It's a little behavioral hack that can help us combat the psychological warfare caused by debt. You can read the original piece at the link above.

Well, I've used the pile of cash three times in the past month. Most notably, I have one particular story to share with you. One of my clients wanted to purchase a new vehicle, around $65,000. After accounting for their trade-in, the remaining amount due was $50,000.

I think we can all agree that $50,000 is a lot of money. Therefore, they naturally decided to finance it. Whoa, whoa, whoa!!!! I was walking alongside them while they painfully and frustratingly paid off a ton of debt, and now they want to go back into $50,000 of debt to buy a vehicle?!?!

"I don't care if you buy this vehicle," I told them. "However, if you decide to buy it, use cash. Please don't fall into this trap again."

"I don't think we would feel comfortable taking $50,000 out of savings to do this," they responded.

"I guess you don't want the vehicle that badly, then." That comment didn't go over well.

They were still waffling when we left the room. That's when I gave them the pile of cash test challenge. Go to the bank, withdraw $50,000, set it on the kitchen table, then decide how important that vehicle is.

It wasn't easy for them to withdraw $50,000 from their bank, but they did it!!! They even joked that it felt like they needed to hire armed bodyguards just to have it in their home.

The result? Here's what they wrote back: "It was an eye-opening experience. To be honest I'm not sure we could ever spend $50,000 on a car ever again after doing that. It puts much in perspective. I think we need more contentment or more humility. Maybe both."

The pile of cash test never fails. Put this one in your toolbelt for a rainy day. It just might come in handy if you're ever in need of a fresh perspective.....or a fun behavioral science experience.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Getting Back Into His Cage

His mental health is eroding quickly. Dark thoughts are starting to seep in. His breaking point might be approaching.

Note: This is a sensitive story, but fortunately for countless readers, I've been granted permission to share it here.

A man asked to meet with me. Mid-40s. Married. Three children. Above-average household income. Average house. Pretty standard lifestyle: not too bougie, but also not perceived as frugal.

Here's the short version of the situation. He's beyond stressed. Finances are causing tremendous friction in his marriage. His wife wants to stay home with the kids, but they can't make it work. He's embarrassed. He feels like a failure. He's miserable. He hates his job. He wakes up each day dreading what's about to happen. He can't leave, though, as his current income exceeds other known options. His mental health is eroding quickly. Dark thoughts are starting to seep in. His breaking point might be approaching.

As our conversation progressed, I started asking him probing questions to identify the true stress points. For several minutes, nothing he said alarmed me.....all normal stuff. Then, we found it.

"Tell me about the vehicles. Do you have any vehicle debt?"

"My truck payment is around $1,300, and my wife's SUV is $800 per month."

There it is! $2,100 per month on vehicle payments alone. All of this pain, suffering, misery, and struggle, only to boil it down to a few key decisions. I challenged him on these decisions.

"Our vehicles aren't nearly as nice as some of our friends and family."

"I'm a truck guy. I can't help that I like nice trucks."

"I want my wife to be safe. We need something reliable."

I have a rhetorical question for you. Do you believe the three sentiments above merit wrecking one's entire life, marriage, financial structure, and mental health? The answer is a resounding NO!!! Of course it's not, but millions of Americans live in this reality daily.

Everything he and his wife have ever dreamed of lives on the other side of these vehicles. These vehicles are cages! They've been snared in the trap. They unknowingly locked themselves in a life they don't want to live. The cage might not have metal bars, but it might as well. I made my case for a different set of decisions, trying to illuminate what an alternate reality could look like: their dream life. However, it requires them to destroy the cages.

After the meeting, I walked outside with him, shook his hand, and watched him get back into his cage. I gotta admit, it was a pretty sweet truck. Clean, fresh wax, enormous in stature. But a cage, nonetheless.

We all have cages. It might not look like a truck, but it's something. My challenge to you today is to look at yourself in the mirror and identify your cage. Something that is (or could) hold you back from living the life you deserve to live. It's an uncomfortable exercise, and not always as obvious as it seems. I've had my share of cages over the years, and I suspect you do, too.

Smash the cage.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Under My Roof

Somewhere in there, I realized that the causes and solutions to all of my problems lived under my roof. I was the common denominator for my crappy situation, and whether I liked it or not, I was responsible for navigating my life to a better situation.

Yesterday, I mentioned being in $236,000 of debt at one point. It was 2008, and I was 27, newly engaged. I had my entire life planned out, all the way down to how many children I would have.....and when. Yeah, talk about being young and naive! Everything was going swimmingly until I walked into work one day and was met by a stranger, a stranger who pulled me into a conference room where I found all of my co-workers. Over the next 30 minutes, we were informed that the company was being shut down and that everyone would soon be fired.

That day was the turning point of my life. That was the day I realized that my way of perceiving and handling money was going to painfully catch up with me, and I would soon lose autonomy over my own life decisions. I had $236,000 of debt that wanted to be paid, and the prospect of no income (worst job market of our generation) was a scary proposition for a young man just a few years into his young career.

Self-pity and victimhood were running at full speed in my mind! I had every excuse in the book why I was done dirty, and I was going to suffer the consequences of other people's decisions. That's when I had a wake-up call....a very harsh and humbling wake-up call.

Somewhere in there, I realized that the causes and solutions to all of my problems lived under my roof. I was the common denominator for my crappy situation, and whether I liked it or not, I was responsible for navigating my life to a better situation. Until that moment, I thought my fortune and failures rested in the hands of outside forces. In other words, personal responsibility played less of a role than luck. That wake-up call changed everything for me.

If my past decisions led me to a place where I had limited life options, then perhaps my current and future decisions could get me to a place with more life options. My new fiancé and I set a new plan for our lives, and that plan involved never repeating that debacle again. We committed to ourselves that we would forevermore perceive money differently and would never again allow finances to dictate our lives.

It took 4.5 years to work our way through the debt mess, but life was so beautiful on the other side. Turns out, my wake-up call was right. The cause of and solution to most of my life's problems lives under my roof.....and it stares at me in the mirror.

The same goes for you. The cause of and solution to your life's problems probably lives under your roof. That's never a fun thing to admit, but once we do, it has the power to change everything. We must own our past decisions and equally own the responsibility for working ourselves toward a new reality. Discipline, humility, and persistence are key. It's not always fun, but there's something so powerful knowing it lives under your roof.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

What Else Are We Supposed to Do?!?!

A friend of a friend recently made an exciting decision: He purchased a new car!!! Everyone around him is so excited. "Congratulations!" exclaimed one person on social media. "Well deserved," quipped another. Silently, I mourned for him. He did exactly what he was supposed to do, and now, he's screwed.

A friend of a friend recently made an exciting decision: He purchased a new car!!! Everyone around him is so excited. "Congratulations!" exclaimed one person on social media. "Well deserved," quipped another. Silently, I mourned for him. He did exactly what he was supposed to do, and now, he's screwed.

He's a young man in his early 20s, with an okay job ($22/hour, full-time). It's not a bad job, but after I tell you the next part, you'll probably cringe. He has a $62,000 loan on his new purchase. I don't know the exact terms of his financing, but it's highly likely that his monthly payment is north of $1,000.

When I asked my friend about this guy's decision, he said something interesting. This young guy was just trying to do what he's supposed to do. He needed a car, new cars cost a lot of money, so he did what he needed to do to buy it. It's not his fault that he doesn't have a higher income. It's not his fault that cars cost so much. It's not his fault that his new payment is going to crush him. This is the way of the world, and he's just trying to survive.

This young man isn't alone. In fact, I'd say more people fall into this line of thinking than not. It's pervasive.....and it's destructive! I regularly meet with folks who are burdened by crushing vehicle loans. Very rarely do they admit there was a mistake made. Instead, they typically do what this young man did: defend it through the lens of what culture says we should do, have to do.

Is there an alternative? Of course there is! Sarah and I haven't had a car loan for the entirety of our 17-year marriage. It's not because we've always had so much money. Rather, it's because we said we would never again have car debt, then made decisions to honor that promise. What does that look like? In our case, only buying vehicles we could afford. I've never paid more than $19,000 for a vehicle, EVER. Here, I'll show you:

Age 16: $7,000 (if I remember correctly) - used debt

Age 17: $2,500 (after totaling above vehicle) - with cash

Age 19: $19,000 (stupid!) - with a LOT of debt (stupid, stupid!!!)

Age 26: $10,000 (reasonable) - with cash

Age 30: $15,000 (car for me) - with cash

Age 35: $18,000 (car for Sarah to fit twin babies) - with cash

Age 36: $16,000 (replacing a car that got totaled) - with cash

Age 42: $9,000 (my fun 350z convertible) - with cash

We'll soon replace Sarah's vehicle that we purchased a decade ago for $18,000, which now has about 250,000 miles. The budget is $25,000 for a used Toyota Sienna. Why used? Because that's the amount we can justifiably afford without going into debt. It's not easy, but it's simple.

At the exact same time, young adults all over America who are making a much lower income than us are spiraling into crippling debt because "that's what we're supposed to do." Please don't fall for the trap. It's not worth it. I promise, it's not worth it!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

A Different Kind of Success

A theme has taken shape in my coaching over the last few weeks. Several families have recently endured a ton of "life." Yeah, let's call it "life." Job losses, medical emergencies, HVAC breakdowns, car problems, unexpected vet bills.....the list goes on. We're talking about thousands or tens of thousands of dollars worth of "life."

A theme has taken shape in my coaching over the last few weeks. Several families have recently endured a ton of "life." Yeah, let's call it "life." Job losses, medical emergencies, HVAC breakdowns, car problems, unexpected vet bills.....the list goes on. We're talking about thousands or tens of thousands of dollars worth of "life."

Needless to say, these couples are discouraged. They had so many goals. Debt payoff goals. Savings goals. Investing goals. Purchase goals. Giving goals. Whatever their goals were, using that money to absorb emergency after emergency wasn't on their wish list.

Despite all that, I view each of these couples as financially successful. Not successful in their established goals, but a different kind of success. In the past, each of these couples would have immediately resorted to debt to pay for these emergencies. The credit cards come out to play. The HELOC takes on a chunk. A new car loan would be in order. Not this time! Today, each of these couples can (and should!) hold their heads high and recognize the fact that they've experienced the brutal realities of life without incurring debt. That's a massive win in my book!!!

I pray each of these families gets back to some form of normal soon, but in the meantime, I will celebrate this massive success of taking multiple punches without punishing their future selves with the burden of debt.

Maybe you're in a season of achieving all the goals you set for yourself. But if not, and like these families, you're experiencing all the bluntness life has to offer, I hope you can create and celebrate a different kind of success. All wins are worth celebrating, even when winning means surviving the onslaught.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Focus, In Practice

Grinding month after month after month without feeling a tangible win is terrible. Inevitably, life happens, expenses pop up, or they get sidetracked.

Crush one thing, then move on to the next. That was the subject of yesterday's post. Focus is a weird thing, and often difficult for us humans to execute. After all, there are many things vying for our time, attention, energy, and resources. However, whether we like it or not, there's simply not enough time, attention, energy, or resources to attack everything.

Today, I want to share some real-life examples of how this concept works through the lens of personal finance. The most common and notable version of this concept I see people shortchanging themselves is debt. Specifically, the payoff of debt. When we try to pay all our debts off at once, we'll likely pay none of them off.

Here's an example of what this looks like, using some nice round numbers for simplicity's sake. A family has ten $1,000 debts, totaling $10,000. This couple determines that it can afford to pay $1,000/month extra toward the debt (above the minimum payments).

Conventional wisdom says that if they pay $100/month toward each debt, they can have their debt paid off after 10 months! That's exciting!!! Here's what that looks like in practice, though:

After 1 month: 0 debts paid off

After 2 months: 0 debts paid off

After 3 months: 0 debts paid off

After 4 months: 0 debts paid off

After 5 months: 0 debts paid off

After 6 months: 0 debts paid off

After 7 months: 0 debts paid off

After 8 months: 0 debts paid off

After 9 months: 0 debts paid off

After 10 months (if everything went perfectly): 10 debts paid off

The gap between month zero and month 10 feels massive. Grinding month after month after month without feeling a tangible win is terrible. Inevitably, life happens, expenses pop up, or they get sidetracked. Failure is likely. Not because they didn't have it in them, but because they lacked focus. Discouragement sets in. A sense of defeat saturates them. Quitting is on the table.

Let's try this again, but with focus as the primary objective. Instead of paying $100/month toward 10 different debts, they decide to focus all $1,000/month on one debt each month. Here's what that strategy looks like:

After 1 month: 1 debt paid off

After 2 months: 2 debts paid off

After 3 months: 3 debts paid off

After 4 months: 4 debts paid off

After 5 months: 5 debts paid off

After 6 months: 6 debts paid off

After 7 months: 7 debts paid off

After 8 months: 8 debts paid off

After 9 months: 9 debts paid off

After 10 months: 10 debts paid off

Will life still get in the way? Probably. However, look at those wins! Almost immediately, this family would experience and benefit from wins. From a psychological perspective, wins matter. Getting a win provides much-needed encouragement, confidence, and motivation to not only keep going, but even step on the gas harder.

This one small shift in perspective can be the difference between complete failure and world domination. Same dollars, same timeline, same commitment. Different focus, different results.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

10 Months For the Rest of Your Life

Imagine this. You're 27, newly married, and recently purchased your first house. Up until now, your entire adult life has been somewhat shadowed by the consumer debt hanging above you: student loans and vehicles.

Imagine this. You're 27 and newly married. Up until now, your entire adult life has been somewhat shadowed by the consumer debt hanging above you: student loans and vehicles. It hasn't felt crippling, but it's an ever-present elephant in the room. Things are going fairly well, but there's a constant suspicion that this whole life thing would be much simpler (and better!) without the debt hovering and constantly absorbing a chunk of your monthly cashflow.

One more detail. With focus and intentionality, this debt could be 100% paid off by the end of this year. In a matter of months, you could forever free yourself from the financial burden you've spent your entire adult life living with. Paying off this debt will be simple, but difficult. It will take discipline, persistence, and sacrifice, but it's very doable.

One of my clients is living in this exact reality. Here's how I recently framed this opportunity to them: "It's 10 months for the rest of your life!"

10 months from now, at the ripe old age of 28, they could put themselves in a position to never again have to deal with the debt. Student loans and car debt gone.....forever! It's a line in the sand moment that will forever be cemented in their story.

Should they do it? Would you do it if you were in their shoes? Speaking as someone who has been in their shoes, and walked alongside dozens of families in similar shoes, I can wholeheartedly testify that it's worth it in every single way. I'm 14 years past the moment Sarah and I paid off ours, and life has never been the same since. It literally changed everything for us.

I think they are going to do it—10 months for the rest of their lives. It won't be easy, but it will be something they will never forget. If you're in a similar situation, I'd give you the same exuberant encouragement I gave them. Run the race, enjoy the fruits: margin, peace, confidence, discipline, and freedom. It's a priceless reward for a job well done.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Crazy Enough to Believe

$118,000 of student loan debt seems overwhelming because, well, it is.

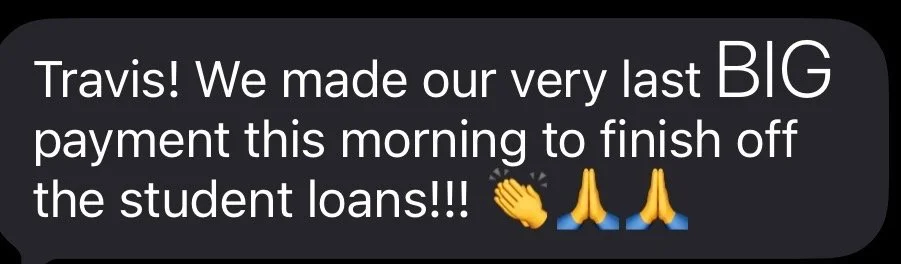

I received the most wonderful text a few days ago. Instead of telling you about it, I'll paste a screenshot for you:

Whoa! Talk about an amazing way to start the day, receiving a dramatically positive life update from a former client. However, I think more context is in order. I haven't seen this client in more than two years. After doing a lot of coaching work, this couple decided they had the tools they needed to win....then promptly kicked me to the curb (which is the goal!). I was grateful for the opportunity to work with them, and firmly believed they would take the reins and crush it going forward.

I knew they were well-positioned to succeed the last time we met, but since I haven't been meeting with them, I really didn't know what was happening behind the curtain. After receiving that text, I immediately opened their file to refresh my memory. I knew they had a TON of debt, but I didn't remember how much. Here's what I discovered. My last meeting with them was 28 months ago, when they were sitting on about $118,000 in student loan debt. Ouch!

Seeing the numbers on that spreadsheet took me back to those coaching meetings. $118,000 of student loan debt seems overwhelming because, well, it is. It was intense! However, at the same time, this couple didn't seem rattled. Instead, they were surprisingly optimistic. They were crazy enough to believe they could pay it off. Frankly, that's the secret. The only way to attack $118,000 of student loan debt is to violently attack $118,000 of student loan debt, month by month. This couple had faith, discipline, unity, and perseverance. They were also crazy enough to believe they could do it!

Of all the principles I've learned from watching families (including my own) get out of large amounts of debt, the power of being crazy enough to believe is often the make-or-break factor of success. Conventional wisdom says we'll never be able to pay off $118,000 in student loan debt. If you believe that's true, you surely won't. However, if you're even a fraction as crazy as this couple to actually believe it's possible, not only will it be possible, but inevitable.

I couldn't be happier for this family. They are needle-mover world-changers, and I have a feeling there's about to be a wave of generosity and impact in their wake. They deserve to live in this reality, not because of entitlement, but because of the work they put into making it happen. $118,000 of debt, 28 months. Unreal!

Whatever absurd goal you're carrying with you today, there are a lot of factors in play that will determine whether or not you achieve it. Are you crazy enough to believe you can? The answer to that question will speak volumes about what's about to happen.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

No Right Time

"This isn't the right time." What do you mean this isn't the right time?!?! You are broke, miserable, and relationally hanging on by a thread. Doesn't this time seem as good as any?

A young couple was hurting. Deeply in debt, tension in the marriage, and jobs they loathed. They felt stuck. They wanted a better life, but it felt utterly unattainable. After about 30 minutes, we visually mapped on the whiteboard how they could simply (but not easily) free themselves from this debt and the life they feel stuck in. All it would take is 15 months, a ton of intentionality, a dose of humility, and a bunch of discipline.

"This isn't the right time."

What do you mean this isn't the right time?!?! You are broke, miserable, and relationally hanging on by a thread. Doesn't this time seem as good as any?

"We have too much going on right now. Maybe in a year or two when things line up a little better."

That's when I had to break the news to them. There is no right time. The right time will never come. Their lives will absolutely not get easier. Nothing will line up better. This needle they are hoping to thread doesn't exist.

Literally every month of their life from here until they die will be the wrong time. If that's true, then there's no better time than now! Seriously! Regardless of what you're hoping to accomplish, there is no right time. It might seem like a better time might, possibly, perhaps, maybe be on the horizon......but it's not. There's no such thing. As such, there's no better time than the present!

This is the #1 rule when engaging in our goals, financial or otherwise. If we recognize there really isn't ever going to be a good time, then we might as well start now. Yes, today is a bad day to start; so is tomorrow. So we should probably just get started today.

I can read your mind. You have something you want to do. It's been itching at you. You desperately want to get going, but now's not the right time. I agree, it's not......but no right time will ever exist. Therefore, let's get started.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Selling Your Future

Every dollar invested gains control of a piece of our future. Conversely, every dollar of debt we incur gives up control of a piece of our future.

"I feel like we sold our souls."

Those were the harsh and horrifying words from a couple I met with. The topic of discussion? Their multitude of debts: student loans, cars, and a HELOC. They followed society's game plan perfectly, and here they sit, living a reality millions of people experience every day.

They got the stuff they wanted and are living the lifestyle they desired, but at what cost? It all felt good in the moment, but at 40, they're starting to gain a sense of clarity. The clarity? It might not have been worth it. As they sit, their options are limited. They had some other dreams in life, but at this point, it all feels so unattainable. The debt weighs heavy.

No, they didn't sell their souls. But in a very tangible and sad way, they sold their future.

Here's how I often look at money. Every dollar invested gains control of a piece of our future. Conversely, every dollar of debt we incur gives up control of a piece of our future. It's a scoreboard that continues to track our progress, but we don't actually know what the score is until decades later. By the time our fate becomes apparent, it's too late to alter it.

Using debt to get what we want now is effectively selling our own future. I believe this about every debt in our lives except the mortgage on our home, but then again, I'm starting to see people make decisions about home ownership that are destructive to their future as well.

That fat car payment? You're literally driving your future.

The fancy tools, gadgets, and furnishings put on a credit card? Your future will be sitting in a landfill soon.

That pool you installed with the HELOC? You're doing cannonballs into your future.

Every week, I sit face-to-face with couples that are absolutely crushing it on the income front. They make more money than most people can ever imagine. However, month by month, I'm simultaneously watching them lose control of their future. Their present looks so very good, but their future so very scary. And the truth is, it's hard to adequately explain to someone who feels so good about their present that their future looks bleak. In fact, it's one of the most challenging endeavors I've ever encountered in this career.

No, I don't want people to live in squalor. I don't want people to live a life void of wants or fun. I'm not trying to be the enjoyment police. If you're a regular reader, you know how much I encourage and advocate for spending money on things that add value to our lives. Instead, I'm trying to warn people about the inadvertent dangers that lurk ahead when we voluntarily give up control of pieces of our future. Bit by bit, drip by drip. It feels so innocent today, but one day, unfortunately, it might not be.

Seize today! Wring every ounce of meaning and awesomeness out of today. But please don't sell your future. Your future self deserves better.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

The Cost of Being Human

You know how I know it's true? She's human, and we humans have this psychological quirk. That doesn't mean we're dumb or irresponsible......we're human. It doesn't mean we're being reckless or foolish.....we're human.

I received dozens of messages on the heels of my recent credit card article. In the post, I highlighted how 46% of credit card holders (approximately 100 million people in America) don't pay off their balance every month. In other words, nearly half of the people who use credit cards carry debt due to the use of said credit cards. This is a pretty shocking statistic considering every single person who uses a credit card claims they never carry a balance.

I have to admit, though, that if 46% of people carry a credit card balance, it means that 54% of people don't carry a credit card balance. If you live in this camp, chances are you're more than happy to throw that fact in my face right about now. I've written about this topic before and podcasted extensively about it, but there's a sneaky little behavioral science quirk that plays a bigger role in our lives than we'd like to admit.

Even if we never pay a single penny of interest or carry a balance from month to month, we're still subject to the psychological consequences of disconnecting the purchase from the payment. When we buy something today that we don't actually pay for until upwards of a month from now, it impairs our decision-making. This is a scientifically proven concept. In fact, studies have shown that we spend 10%-30% more when using a credit card than we would have if we used cash. Further, we're more apt to make purchases that we wouldn't have made at all. Ouch!

Here's an interesting note I received from a blog reader who has successfully managed to use a credit card for many decades without carrying a balance or accruing any interest:

"I always thought I was using our one credit card responsibly because we paid it off every month. That is, until my wise daughter suggested I look at my list of credit card purchases and see how many I would have made if I had to pay cash for them. I realized I made a lot more impulsive purchases when I use a credit card, even though I never carry over a balance from month to month."

This. This right here. She's so, so right. I applaud her humility and vulnerability in this statement. You know how I know it's true? She's human, and we humans have this psychological quirk. That doesn't mean we're dumb or irresponsible......we're human. It doesn't mean we're being reckless or foolish.....we're human.

I'm not mad at people for using credit cards. I don't look down upon them. Yes, people can still be successful when using them. At the same time, my mission here is to open people's eyes to the unseen costs and hidden psychological forces of utilizing this little piece of plastic technology. Nothing is free, as they say.

I, for one, will continue to live a life free from the behavioral and financial consequences of credit cards, and I'd encourage you to do the same. Either way, press on and have a great weekend!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

No Room For Hypocrisy

In short, I have a one-word answer for this: hypocrisy. Hypocrisy prevents me from using credit cards. If I'm publicly and privately criticizing the use of credit cards, warning of the risks, in what world would it make sense for me to use one myself?

One of our longtime readers posed an interesting question to me after my recent rant about credit cards. I'll paraphrase her thoughtful question. How can I be so disciplined with budgeting but can't be so with a credit card? In other words, what's preventing me from properly handling credit cards like I handle all the other areas of personal finance?

In short, I have a one-word answer for this: hypocrisy. Hypocrisy prevents me from using credit cards. If I'm publicly and privately criticizing the use of credit cards, warning of the risks, in what world would it make sense for me to use one myself?

Approximately 15 years ago, Sarah and I were at dinner together. When the bill arrived at our table, I whipped out my credit card and slid it into the little black folio. As the waitress walked away with my card, Sarah looked at me and said, "You know you're the world's biggest hypocrite, right?"

Uhhhhhhhh, what?!?! "You tell everyone they shouldn't use a credit card, and here you are using a credit card."

Pot, meet kettle. Ouch. I could use a credit card because I understood the perils, pitfalls, and behavioral science implications. Yet, at the same time, my actions only proved that I was a hypocrite. The moment we got home, I pulled out a pair of scissors and cut up the card. Sarah was right, I was a giant hypocrite. Never again, though. I have no room in my life for hypocrisy, and if I believe in what I teach, I should eat my own cooking.

Can people use credit cards responsibly? Yeah, some can; very few can. A rare minority can. It reminds me of the famous Jeff Goldblum quote from Jurassic Park: "Your scientists were so preoccupied with whether or not they could, they didn't stop to think if they should."

Could vs. should is an interesting topic to think about. There are a lot of things I CAN do, but it doesn't mean I SHOULD do them. If we want to hold people to higher standards, we need to hold ourselves to a higher standard. This has become one of the biggest principles in my coaching. I will NEVER ask someone to do something that I'm not already doing in my own life. When I teach people how to invest, it's exactly how I invest. When I help people get life insurance, it's the exact principle I follow. When I show people how to give, it's exactly how I practice giving. When I teach people how to prepare for their children's college, it's exactly how I think through my own children's education.

I never tell people what to think, but I teach them how to think. Regardless of each family's individual values, beliefs, and aspirations, these concepts and principles allow them to implement wise and thoughtful decisions in their own lives. That begins with building trust, and trust is built on a lack of hypocrisy.

Just because we can, it doesn't mean we should. This applies to so many areas of life, so today I'll let you extrapolate it to wherever it needs to be implemented in your life. Have an awesome day!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

The Oz Next Door

"You throw around all these statistics, but there's literally not one person in my life who is struggling with credit card debt."

Oh man, I took some HEAT heat after yesterday's post. Yes, some productive feedback, for sure. But the heat was hot. One particular criticism caught my eye:

"You throw around all these statistics, but there's literally not one person in my life who is struggling with credit card debt."

I'm sure you've seen The Wizard of Oz; it's a classic! My favorite scene in the movie is after 93 minutes of being made to believe Oz is so great and powerful, the curtain is pulled back to expose him as a fraud. It turns out he used smoke and mirrors to portray himself as this great and powerful wizard, when the truth was he was a frail old man.

This might come as a shock to some, but you probably have an Oz living next door to you. You probably have an Oz in the cubicle next to you at work. You probably have an Oz in your family. That fancy-looking couple at church? Possibly an Oz. The "rich" person you tend to get jealous of? Possibly an Oz.

In my work, I have the privilege of seeing behind the curtain of hundreds of households. The world sees what it sees, and in many cases, they see a great and powerful wizard. Unfortunately, what's really behind the curtain is a proverbial frail old man.

What appears to be wealth is really debt.

What appears to be freedom is really slavery.

What appears to be success is really destruction.

What appears to be wisdom is really tomfoolery.

What appears to be sturdy is really fragile.

I could tell you story after story after story of wealthy-looking people who appear to be the definition of success, but are on the brink of utter destruction.

I've witnessed so many tears from people who make $500,000+ per year, live in mansions, drive luxury vehicles, have a social media timeline full of exotic travel pictures, and have status in their community.

In many of these cases, credit cards aren't what directly propelled them into a financial spiral. Their car loans, lifestyle creep, and hefty mortgages did the initial damage. However, almost every one of these situations eventually results in brutal credit card debt. The credit cards become the symptoms of destruction, and the boat anchor that prevents the ship from ever floating again. They can always sell a car or a house, but there are only two ways out of credit card debt: grind it out or file for bankruptcy. It's the silent killer that's draining the hopes and dreams of an entire generation.

You absolutely know dozens of people who are deeply impacted by credit card debt; you just don't know which ones. They are hiding behind their curtains, hoping to maintain their appearance of being a great and powerful wizard.

Moral of the story: Never be jealous of the people around us. They might be an Oz. Instead, live with a posture of contentment and humility, pursue meaning, and never allow the desire for more to pollute your peace.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Just Pay It Off Each Month, They Say

Credit cards are our best friends... until they become our worst enemies. Unfortunately, we never know when that tipping point will come. One minute we're fine, and next our financial life is ruined. I've been on a crusade against credit cards for nearly 15 years, and there's no better topic to stir up the hate train than to discuss my disdain for them.

Credit cards are our best friends... until they become our worst enemies. Unfortunately, we never know when that tipping point will come. One minute we're fine, and next our financial life is ruined. I've been on a crusade against credit cards for nearly 15 years, and there's no better topic to stir up the hate train than to discuss my disdain for them.

First, no, I don't use a credit card. I used one from age 18 to 30. Then, after much research about the cold, hard data, the predatory nature of the product, and the behavioral science implications, I drew a line in the sand and decided to permanently ban them from my life.

A quick FAQ:

What do you use if you don't have a credit card? We use debit cards.

What about the risk of your card getting stolen? Our cards have been stolen multiple times. It's annoying, but you aren't liable for loss.

What about travel? You NEED a credit card for travel. I've traveled to more than 30 countries with only a debit card. It works great.

Don't you need a credit card to book a hotel room? No.

Don't you need a credit card to rent a car? Some companies, yes; other companies, no.

You use your debit card for online shopping?!?! Haha, yes. Every single day of my life.

Don't you want to build credit? No. I haven't had a credit score since 2015.

Here's one of the primary arguments FOR using a credit card (primarily to collect those sweet, sweet points): "Just put everything on a credit card and pay it off every month. Just be responsible!"

The truth is, that's not what people do. In theory, yes, that's a great idea. However, in practice, the data shows something much different. My coaching experience already tells me this is true, but data recently released by the Federal Reserve paints a clearer picture.

There are currently an estimated 268 million adults living in the United States.

81% of those adults, or 217 million people, own a credit card.

Of the people who own a credit card, 46% (100 million people) carry a balance each month.

"Just put everything on a credit card and pay it off every month. Just be responsible!"

This principle works really, really well......until it doesn't. And today, unfortunately, 100 million adults in the U.S. are (secretly) living in the "until it doesn't" reality. This is ripping families and lives apart!

"Well, it must be the young, irresponsible people who are being stupid with their credit cards."

The demographic most affected by carrying credit card balances is 45-59-year-olds, with 54% of cardholders carrying a balance from month to month. "Only" 44% of 18-29-year-olds carry a balance.

"Well, if people made more money, they would pay off their credit cards instead of carrying a balance."

Even in households earning $100,000 or more per year, 38% of cardholders carry a balance from month to month.

Credit cards aren't a math problem; they are a human problem. Credit cards aren't a responsibility problem; they are a psychological problem.

Something to think about today.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Screwing Up My Own Recipe

In other words, I lived a "normal" life and fell right into the hands of our culture's toxic perspectives. I was the epitome of our modern materialism.

Today's post is inspired by one of our readers from Guatemala, who emailed me regarding yesterday's post. Turns out, most of us totally botched the recipe I laid out yesterday. And by most, I'm including myself. In fact, I botched it hard! So hard, in fact, that I ended up being a victim of an out-of-state involuntary relocation because my finances didn't provide the margin for me to make my own choices.

Just in case you all somehow think I'm some financial wiz kid who has always got it right, here are some of the costly decisions I made between the ages of 16 and 27 (i.e., all the ways I violated and brutalized the recipe I laid out in yesterday's post):

I had my first car loan at age 15. Fifteen! It was a pretty sweet Camaro that I painted Carolina Blue.

Instead of choosing any number of in-state colleges, I elected to pay 4x as much as necessary to attend an out-of-state school.

I signed up for my first credit card one month into college, effectively delinking my income from my spending. I never carried a balance, but using a credit card no doubt had a psychological impact on my spending.

During my second year of college, I sold my reliable, paid-off car and purchased a $19,000 Acura Integra. Very sweet car, but to this day, it's the most expensive car I've ever purchased. Think about that. The car I bought 24 years ago, with a poor college kid's income, was the most expensive car I've ever purchased. Just wow!

I bought my first house two years after graduating from college. I felt the cultural pressure to move quickly and shoot high, and I certainly met the mark on both.

My giving was approximately zero. And by zero, I'm not sure it ever even crossed my mind! That young Travis was selfish!

I kept up with the Jonses the best I could. I didn't know if I would win the race, but I was sure giving it my best effort.

I used debt for everything, all the way down to my wife's engagement ring. By the time my company shut down and I was involuntarily relocated, my debt had ballooned to $236,000.

Meaning? What's that?!?! My goal was to make as much money as possible, enjoy said money, and invest the rest effectively so I would have even more money to enjoy later.

In other words, I lived a "normal" life and fell right into the hands of our culture's toxic perspectives. I was the epitome of our modern materialism.

There was always hope for me, and fortunately, I eventually became humble (and humbled!) enough to change. Regardless of where you are or what mistakes you've made (or still making), there's always hope for you, too! It's never too late to make meaningful shifts. A few chapters of your story have already been written, but great books aren't defined by the beginning. In fact, the best stories get progressively better as the adventure unfolds, and your story is no different. Here's to the next chapter!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Right or Luxury?

Buying a new vehicle is a luxury, not a right. However, since this is America and our culture is so twisted, we've conditioned the masses to believe that everyone deserves to buy a new vehicle. The truth is, we don't inherently deserve to go out and buy a new vehicle just because everyone else is doing it.

As expected, yesterday's post offended a fair number of people. We Americans love our cars, and the mere suggestion that we shouldn't have a car payment sounds as absurd as me suggesting we ought to live our day-to-day lives naked like a bunch of crazy nudists. That suggestion would sound absurd to nearly everyone, and for many reasons, so too is my suggestion that we should all live without vehicle payments.

One of my friends was particularly peeved by my absurdity and decided to call me.

"Travis, do you know how expensive cars are these days?!?! It's practically impossible for most people to buy a new car without getting a loan."

"Yeah, you're right."

"So how do you expect most people to buy a new car without having a payment?"

"I don't."

My friend is absolutely correct! New cars are brutally expensive. Based on recently published data, the average price of a new vehicle during the first half of 2025 was approximately $49,000 (with an average payment of $745/month). Therefore, we have two options: 1) We fork over $49,000 of cash, or 2) We elect for big, fat car payments.

Therefore, my friend makes a good point. It's nearly impossible for most people to buy a new vehicle without large payments. Or.....or.....or, hear me out. Perhaps we can put a third option on the table: 3) Don't buy a new car!

Buying a new vehicle is a luxury, not a right. However, since this is America and our culture is so twisted, we've conditioned the masses to believe that everyone deserves to buy a new vehicle. The truth is, we don't inherently deserve to go out and buy a new vehicle just because everyone else is doing it.

I've never owned a new vehicle in my life, as I don't believe the lie that buying a new vehicle is a right (or a good decision). Even if I could buy a new vehicle, I doubt I ever would. One of the consequences of my decision not to buy a new vehicle is that I haven't had a car loan for more than 17 years. Here's a rough history of all the vehicles Sarah and I have purchased in the past 17 years:

2008: Used Honda Accord - $15,000

2013: Used Nissan Altima - $16,500

2017: Used Toyota Highlander - $15,000

2018: Used Nissan Altima - $15,500

2024: Used Nissan 350Z - $9,000

Today, our three vehicles have a combined value of $20,000-$25,000.....COMBINED! Would we like to upgrade our vehicles? Of course! And we probably will later this year, but going into debt to do so is an absolute non-starter. We'll buy whatever vehicle we can afford with the cash we have saved for said purchase. Buying new vehicles isn't a right; it's a luxury.

On the flip side, you wouldn't believe the number of people who make $50,000 per year who drive new $50,000 vehicles. The big, fat car payments people are signing up for are crushing their ability to make progress in their financial lives. It's madness!

I again invite you to join the movement. Let's live out a different reality for people to witness. A debt-free reality where we buy vehicles we can afford and live meaningful lives that are far richer than being a slave to our payments. Let's go!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Normalizing Negligence

Today, we're paying tribute to category #4, car dealership monthly payment interviews. I first discovered this trend a few years ago, and I'm overjoyed to see it pick up momentum over the last few years. In short, this is a trend where someone working at a car dealership will walk around the premises with a microphone, asking employees what they drive and what their monthly payment is.

You know how social media algorithms have a way of slotting us into specific niches? My niches have evolved over time, but at the moment, my four favorite niches are as follows:

Flat Earthers - You GOTTA check it out!

Tinned Fish - Who doesn't love a good tinned fish?!?!

All things Twenty One Pilots

Car Dealership Monthly Payment Interviews

Today, we're paying tribute to category #4, car dealership monthly payment interviews. I first discovered this trend a few years ago, and I'm overjoyed to see it pick up momentum over the last few years. In short, this is a trend where someone working at a car dealership will walk around the premises with a microphone, asking employees what they drive and what their monthly payment is.

Here's one example! If you want the Cliff Notes version, here are the results (each employee’s monthly vehicle payment):

$744

$726

$600

$1,000

$935

$0

$700

$0

$700

$400

$415

$469

$1,080

$593

$0

Or, this one:

$700

$1,400

$750

$634

$520

$706

$340

$360

$0

$2,650

$1,500

$700

$675

$0

$1,600

$0

$900

$485

Finally, we'll end with this gem:

$950

$730

$0

$404

$0

$700

$450

$600

Those are just four random videos. There are hundreds of them out there, and I just blindly clicked on four for this little exercise. Here's the lay of the land:

Out of the 41 people surveyed, 80% of them (all but 8) have monthly payments. Translation: Only 20% are debt-free on their vehicles.

Six people (15%) have monthly payments of $1,000+.

Only six people (15%) have monthly payments below $500.

Of the 33 people with monthly payments, the average payment is $791/month.

First, let me say that I'm not condemning any of these people. I don't think they are dumb, nor do I have any negative opinions about them personally. I could easily have clicked on four other random videos and achieved the same results. These people are normal. While these numbers might shock some of you or create skepticism, I can assure you they closely mimic my experience working with hundreds of families.

It's "normal," and that's the problem. In recent months, as the algorithms have pushed me more of these amazing videos, I've started asking myself the question, "Why?" Why are car dealerships doing this at scale? What's the objective of this social media strategy?

Then, it dawned on me, the proverbial light bulb over my head. They are systematically normalizing negligence. If their employees have big, fat monthly payments, and are presumably industry experts, then it normalizes the idea of having big, fat monthly payments. Again, they aren't bad people. They are just normal people, living normal lives, boosting the momentum for other people to live normal lives as well. And in America, "normal" means having big, fat car payments.

Today, I propose we normalize prudence, humility, contentment, and personal responsibility. There's no reason a single person should have a car payment. None. Will you join me in the fight? I can't do it alone, and luckily, I don't have to. Let's shift the momentum to a better way of living!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.